I saw Seth's blog post about investing in land deals through a self-directed Roth IRA (https://retipster.com/self-dir...), and I wondered if anyone has any additional thoughts or recommendations on this? For example, has anyone had any particularly good or bad experiences in terms of level of service received from the different custodian options, or have any knowledge of how some of their fee structures might compare?

I see Seth included a list of several custodians and I haven't done a direct comparison yet, but I know with all long-term investment accounts, small differences in fees can add up to a large impact over time.

Does anyone have experience, good or bad, with Horizon Trust?

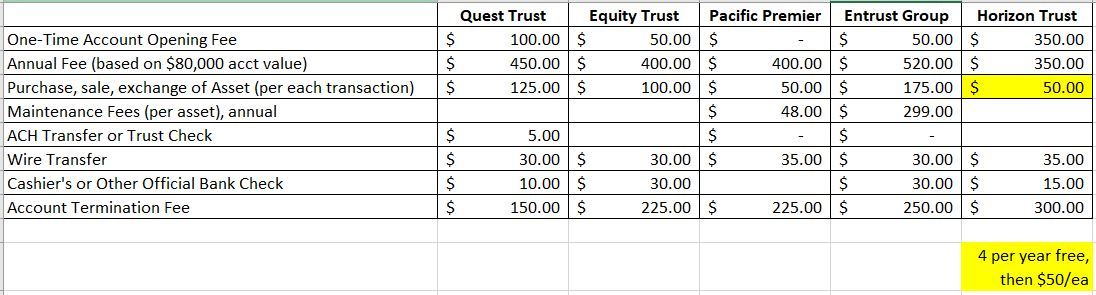

In case anyone is interested, I tried to find and interpret the fee schedules for the five self-directed IRA custodian services mentioned in the blog post I linked above.

Don't take my word for it on these numbers, because I can't guarantee that the documents I found are necessarily the company's current fee schedule in all cases, plus there definitely seemed to be no small degree of interpretation and apples-and-oranges effect in trying to force a comparison in some categories.

Also, Quest and Horizon, at least, offer some alternative account options where you can pay some version of fixed fees or higher minimum/annual fee, in exchange for lower sliding-scale account fees, or no per-transaction fees, etc. Horizon's was the most difficult fee schedule to find (I ended up having to Google it, after failing to find an obvious link for it by browsing their site), but if I I found the correct and current one, and if I'm interpreting it right, it seems like if you anticipate having a upper-5-figure (or higher) account value, and having relatively frequent buy/sell transactions per year, they might have the lowest effective cost, if you go with their Platinum plan, which is an alternative price structure that I did not break down in this table.

I've got a "checkbook controlled" SDIRA from IRA Financial. They offer both checkbook and custodian controlled IRAs The difference between their checkbook-controlled IRA and a more traditional custodian-controlled IRA is the addition of an LLC. The IRA owns an LLC and moves all of its assets into it. You have 100% control of the LLC as it’s manager. You can do land deals through this entity just like you would your land business. You don’t have to ask permission of the custodian every time you do a deal and the custodian is not on title. It makes it very clean to do land deals.

But it’s way more expensive to set up ($1,000). The annual fees seem to be cheaper than traditional SDIRA’s, only $180 a year. But you have to factor in the annual cost of the LLC, which you have maintain and pay for yourself.

Thanks @billwalker! That type of SDIRA was not on my radar, but it sounds awesome. Just to confirm, with this approach, not only do you not need to wait for the Custodian to take actions on your behalf, but are you saying you also don't have to pay the SDIRA service provider any type of per-transaction fee every time that you buy/sell/make-a-deposit/etc. on properties? If so, it seems like the higher setup fee could be recouped pretty quickly based on the per-transaction fees I'm seeing with those other providers, which double if you're generally flipping (buying & reselling quickly).

Regarding the SDIRA's LLC, can someone with experience talk about the accounting costs for this? I am VERY interested in using a Roth SDIRA as a structure for buying & selling land, but fearful of the hidden costs of IRS rules for tracking every transaction, and the subsequent tax return costs for a CPA to prepare the return for the SDIRA's LLC. I know that every CPA has their own rates, but I'm looking for an order of magnitude number from those of you that have already experienced a tax return for their SDIRA LLC. This "fear of the unknown" that's holding me back! The SDIRA companies that I've spoke with won't give me a legitimate answer.

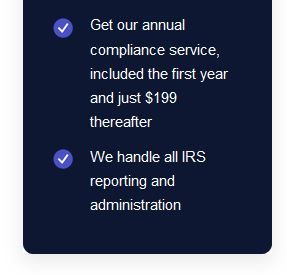

I hear ya, @PaulB. I'm in the same boat and don't have any personal experience with this yet, either, but I did see this on the website for the company that @billwalker mentioned above, IRA Financial Group:

If they do a reasonable amount of hand-holding, especially with first-timers, then I think this will probably be the direction I'll go, unless others have any really positive experiences with a lower-cost provider that offers similar "checkbook controlled" structure.

I just got a property under contract this morning, with a closing not-later-than date in January listed in the PSA, and it will hopefully be a 300% to 400% ROI deal so I'd really like to get that in a Roth.

Edit: The picture doesn't seem to be coming through with my post, so if you're curious, check out the page Bill linked to above. Towards the bottom it says:

Get our annual compliance service, included the first year and just $199 thereafter

I have two checkbook SDIRA's: one with Entrust and one with Horizon. Entrust may not be doing checkbook LLC's anymore, and Horizon is comparatively in the dark ages, when it comes to its portal and support. In my experience, the SDIRA custodians know the legal and tax landmines and will stay clear of those issues; they won't answer the hard questions. When it comes to land flipping, and Seth's post may have touched on this, you want to avoid being in the "trade or business" of flipping land. Owning real estate is allowed, and you can buy and sell land as an investor, but you can't be a land flipper, who routinely and regularly sells land. There is not much guidance on this issue from the IRS, but if you are deemed to be in the "trade or business" of flipping land, the gains are subject to UBIT (taxes). You also need to steer clear of providing services for your SDIRA and the prohibited transactions.

I do this as well. Yes, I do recommend this strategy as an option. I kept looking at the returns in my land business vs. my returns in my IRA and it as a no-brainer. So I moved a small amount to try it and so far I'm pleased. But only do this if you are and experienced, full-time investor. I wouldn't recommend this for a rookie. You need to be an experienced land investor and also understand the tax risk you are facing if you don't follow the rules.

I also use IRA Financial Group. They seemed straight forward and I don't need a lot of hand holding. Been with them for over a year, but have only done 1 transaction as I'm being careful. Would I recommend then? meh. They seemed to be less expensive than the other vendors I interviewed. But they are quick to ask for their next payment and slow to respond and provide service. They take a mass market, cookie-cutter approach. As an example, I have some transactional questions right now. I requested to speak with someone. That has taken 2 weeks, and I'm now on my 4th person because the first 3 either wouldn't respond or couldn't answer my questions. But I think I finally have the right one to answer my questions and we expect to speak soon.

@dl7573 I setup a self directed IRA with Quest. There was no application fee, and yearly fees weren't too bad. I am keeping my funds in my IRA until its time to rollover. I am also considering the checkbook LLC via directedira.com I utilize their tax attorney consultation services, and looking at their options for more flexibility.

In case anyone else is looking into options for this, as well, I wanted to provide an update on what I'm seeing. I'm currently leaning towards setting up a self-directed Solo 401k plan. From what I'm reading, it sounds like it has the direct control advantages of a checkbook IRA (no relying upon, and paying, a Custodian to make every transaction like you do with the Custodian self-directed IRA), without the on-going costs of having to set up a dedicated LLC like you do with a checkbook IRA. Plus, the annual max. contribution limits are higher for a 401k than an IRA.

To go this route, you need to have some type of self-employment, and my wife and I already have an on-going side-hustle business, not related to land investing. In fact, we've already established a traditional Solo 401k with Fidelity under that business, so I think the key questions that I need to get answered by a professional at this point are whether we can have two separate 401k's through the same business (and the same participant), and if so, how our annual contribution caps might be limited (hopefully not) by the business's amount of profit, which I know is an issue for maximizing tax-deferred (traditional) 401k contributions, but I'm hoping maybe doesn't affect Roth contributions(?). We'll see.

@PaulB The SDIRA files an informational return, form 5498, and your custodian should handle that for you. You report the fair market value and any contributions or withdrawals you've made. I'm still unclear on exactly how you value the real estate in your account at the end of the year. Is it basis, or do you need an appraisal? I've heard different things.Other than that, the account does not have to file a tax return.

I saw that you touched on the 401k loan feature. Have you taken advantage of that yourself? I think that it sounds good, but I'm also wondering about some of the details. I know the conventional wisdom (among non-real estate investors) is that loans from, and paid back to, a Traditional 401k account can be a bad deal because while you are paying interest to yourself rather than a bank (which is good), you're also repaying the loan with after-tax dollars into a tax-deferred account, which basically creates double-taxation on your loan repayment (principal plus interest). So I'm wondering if you can direct your loan repayments specifically into the Roth portion of a Solo 401k, to avoid that double-taxation. I'm in the process of setting up my Solo 401k with IRA Financial now, and their rep said that you can put your after-tax loan repayment into Roth, but I'm not sure if she really knew what I was asking, or why it matters.

I saw that they also allow you to specify (when you're creating your plan) how you want your loan terms to work; which is awesome, but I guess I'd probably rather have either a 0% loan interest or a very high interest rate (paid to myself), depending on the answer to the point I raised above. Until I figure that out for sure, I just opted for Prime + 0%.

I’m in the process of taking a loan right now. It’s a super simple process. They gave me a form to fill out and all I have to do is sign it, file it away, and write myself a check. From what I understand, by law you have to charge yourself some interest. I think it has to be at least Prime and no higher than your state’s maximum interest. I plan to charge myself Prime.

You can set up both a traditional and Roth in the same 401(k). I don't have a Roth component. When I talked to IRA Financial, they said you could hold both in the same checking account or set up separate bank accounts. If you keep it all in one account, you should keep very good records. This is all conjecture, but I think if you have both accounts in the same checking account, you might have to treat it like a “fund”. Investments would be allocated between the “investors”, i.e. your two accounts. That would probably apply to the loan too. When you pay yourself back your payment is allocated between the accounts, at a ratio of the account values at the time you made the loan. I’m just guessing about this though. I have no idea. I imagine that if you had two separate checking accounts, you could just loan the money out of the Roth checking account and pay it back to the same account?

Thanks @billwalker, that's a great idea about maintaining separate bank accounts for Roth vs. Traditional balance. All these things that I haven't had to think about during years of being only a Participant in other employers' 401k plans.

I just started following this thread, and wanted to say thanks to all of you for the great info! I’m thinking of shifting IRA funds into something more productive, but want to avoid all the land mines. Anyone have an opinion of Anderson Advisors or Damien Lupo?