In this episode, I’m joined once again by Vernon Henry, a land investor and former professional landman with over 20 years of experience in mineral rights.

If you’ve ever bought or sold land and wondered, Do I own the mineral rights, or could an energy company drill on my property? This episode is for you.

Vernon breaks down the complex world of mineral rights into simple, actionable knowledge. We cover:

- What mineral rights actually are

- How they’re severed from surface rights

- Vertical and horizontal severance

- How to determine if you own the minerals

- How oil companies pool units

- Why landowners receive royalties

- How to value mineral rights

- Where to sell or buy mineral rights

- What to do if your property sits above valuable resources

This is a must-listen for anyone in land investing, real estate, or mineral acquisition.

Links and Resources

- AcreEquityFunding.com (Vernon's Website)

- Mineral Rights for Land Investors (FREE PDF Download!)

- USMineralExchange.com

- EnergyDomain.com

- EnergyNet.com

- Oil & Gas Asset Clearinghouse

- Landman.org (AAPL)

- Landgate.com

- 167: 1031 Exchanges for Land Investors

- WellDatabase.com

- Texas Railroad Commission GIS Website

Key Takeaways

In this episode, you will:

- Learn how mineral rights are separate from surface rights and may not transfer with your land deed, even if the title appears clear.

- Discover that mineral rights owners have dominant legal rights over surface owners and can access their minerals through your property with compensation.

- Understand that mineral rights require specialized title searches going back to original government patents, which regular title companies don't perform.

- Find out about marketplaces like EnergyNet and U.S. Mineral Exchange for buying/selling mineral rights, plus how to hire landmen for research.

- Realize that mineral rights can significantly increase your land's value through lease bonuses and 20-25% royalty payments from production.

Episode Transcript

Mineral Rights Q&A: Ownership and Title Basics

Are mineral deeds a completely separate document from a normal warranty deed, or are the two ever combined?

Mineral deeds can be separate or included in a warranty deed. Unless specifically excluded, mineral rights will convey to the Grantee in a General Warranty Deed. If they're severed, a mineral deed (or reservation clause) is typically used to convey (or retain) just the subsurface rights.

Over time, mineral rights may be reserved during property transfers, so by the time a buyer purchases a property today, the mineral rights may have been reserved one or more generations earlier. This is reflected in the chain of title, which shows how ownership of both the surface and minerals has changed over time. It's common to see surface and mineral estates split decades ago.

If you currently own both the surface and the mineral rights, you can reserve your minerals when conveying the surface. To do this, you must include a reservation clause in the deed at the time of sale. Once recorded, that reservation becomes part of the official record and remains with you unless you later transfer or sell those mineral rights separately.

How far down into the earth do mineral rights go unless specified otherwise?

Unless otherwise limited by contract or law, mineral rights extend to the center of the Earth. However, they can be limited by depth (e.g., “rights below 5,000 feet”).

In practical terms, oil and gas development rarely goes deeper than 12,000 to 15,000 feet of total vertical depth. Beyond this depth, the heat and pressure in the subsurface are so extreme that they degrade hydrocarbons and make drilling uneconomical or technically unfeasible. Most commercial oil and gas reservoirs are located between 2,000 and 10,000 feet deep.

Additionally, as you go deeper, hydrocarbons undergo thermal maturation. Oil becomes gas under sufficient heat and pressure, meaning that deeper zones tend to contain natural gas rather than oil. These geological and thermal limits define where mineral rights are likely to hold value based on development potential.

Why would someone carve out a certain depth of mineral rights?

To keep rights to specific formations (e.g., shallow gas) while selling deeper rights or to structure deals with multiple buyers/operators. It's often done to protect potential upside in stacked formations.

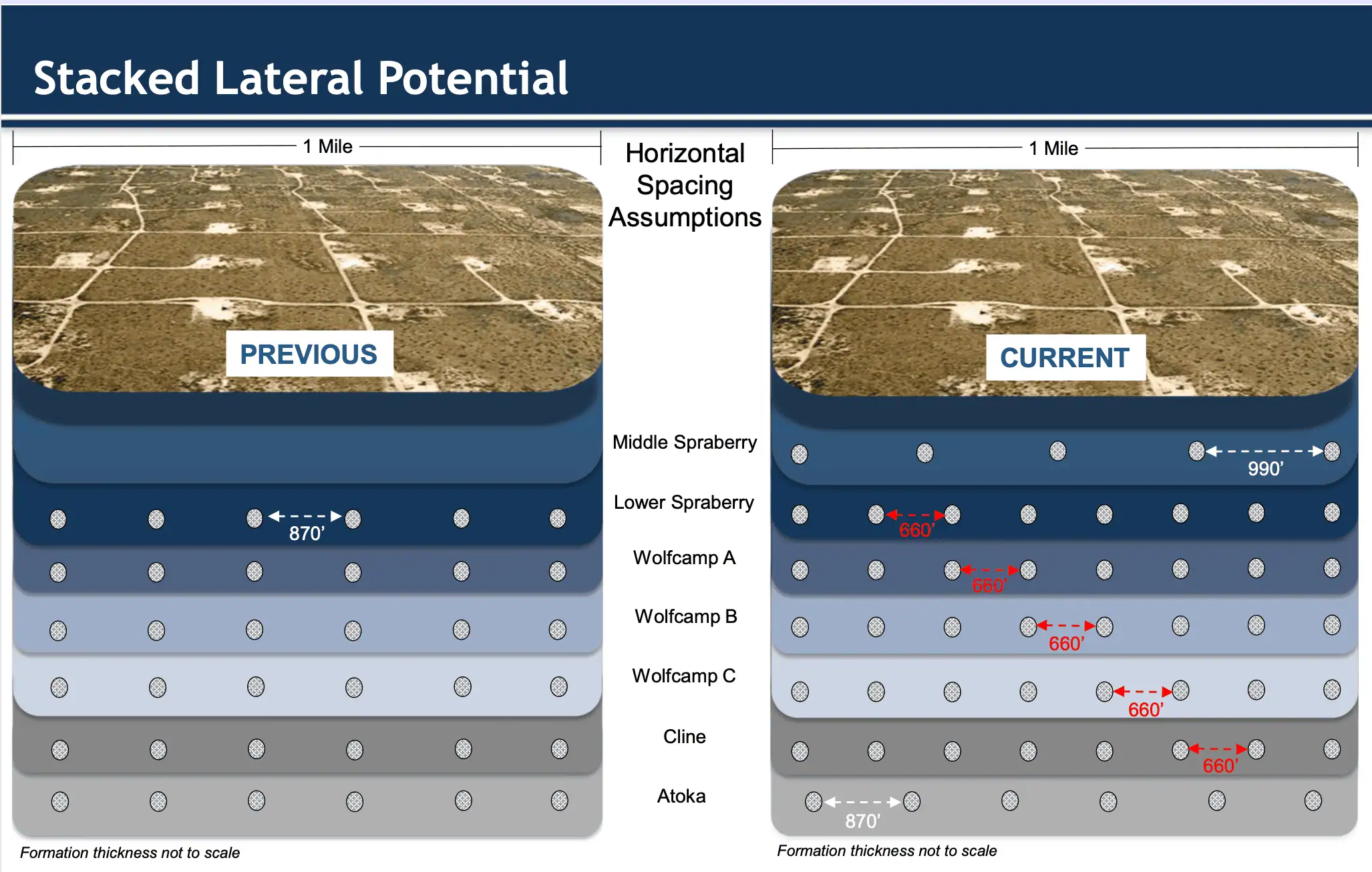

For example, in the Permian Basin, productive formations like the Wolfcamp or Spraberry can range between 6,000 and 10,000 feet in depth. A mineral owner may choose to sell only rights below 7,500 feet to a buyer targeting the Wolfcamp while retaining shallower rights where another operator might eventually drill.

These decisions often hinge on risk tolerance and cash flow needs. Some owners sell rights below a certain depth in exchange for a lump-sum payment, essentially trading potential future royalties for guaranteed money now. Buyers—often specialized mineral acquisition companies—assume the risk that a certain formation will eventually produce, hoping to profit from future lease or royalty income. Others choose to reserve certain depths because they believe those intervals will become economically viable in the future, particularly as technology or market prices evolve.

This kind of depth-based severance is common in basins with stacked pays like the Midland Basin, Delaware Basin, or the DJ Basin, where multiple productive formations exist at varying depths.

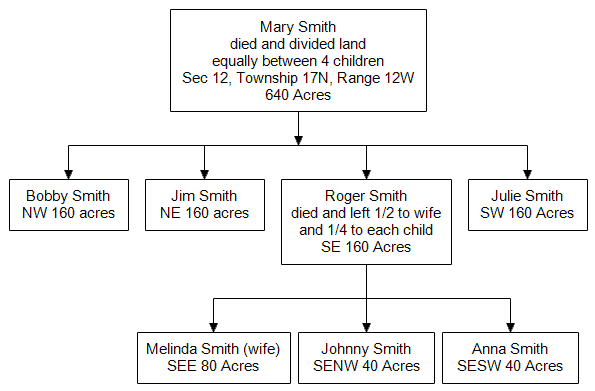

Do mineral title searches have to go back to sovereignty?

Yes—unlike surface title (which often only goes back 40 to 60 years), mineral title must be traced back to sovereignty—meaning the original land patent from the government. That's because mineral rights can be split, reserved, or partially conveyed at any point in the chain of title, and those early decisions affect ownership all the way to the present.

Why this is important:

Let's say in 1890, the federal government patents a 640-acre tract to John Smith. He owns 100% of the minerals. In 1910, John sells the surface but reserves 50% of the mineral rights. From that point on, every subsequent transaction of that tract will only involve a portion of the mineral estate—unless someone explicitly conveys or reunites the full interest (which is rare).

Now imagine that in 1930, one of the mineral owners sells half of their 50% interest to a neighbor. That new interest starts its own chain of title—separate from the original. Then in 1950, that buyer dies and leaves their minerals to three children. Then in 1975, one of those kids sells their 1/6 interest to a different person, etc…

Each of these branching events creates a new “chain” of mineral ownership. So a complete mineral title search has to:

-

-

- Identify every chain created by a severance or transaction

- Trace each chain individually, often through multiple generations, sales, probates, and gifts

- Reconcile all the chains to add up to a full 100% of the mineral estate

-

If you miss even one fractional interest from decades ago, it can throw off ownership today—and you may not even have the legal right to lease, sell, or collect revenue on 100% of the minerals.

This is why mineral title work is often done by landmen, title attorneys, or abstractors who specialize in energy title. It requires a different level of detail than traditional real estate titles—and a lot more digging. You're not just confirming ownership—you're reconstructing the full puzzle over decades or even centuries.

Can you specify certain minerals when conveying or reserving rights?

Yes—mineral rights are often described as a “bundle of sticks,” meaning they can be separated and transferred in many ways. You don't have to sell or reserve all of the mineral rights under a property. Instead, you can carve out specific minerals or specific rights related to those minerals.

You can divide by type of mineral:

When conveying or reserving rights, you can specify:

-

-

- Only oil

- Only gas

- Oil and gas, but not coal

- Hard rock minerals like lithium, copper, or gold

- Aggregates like gravel or sand (if considered a mineral under state law)

-

This type of reservation is common in areas where certain resources are being actively developed—for example, someone might sell the surface and keep the lithium rights because a battery-grade lithium project is moving in nearby.

You can also divide by type of right:

Even within a single mineral estate, different rights can be split up and owned by different parties. These include:

-

-

- Executive rights – The right to negotiate and sign leases with operators

- Bonus rights – The right to receive upfront lease payments

- Royalty rights – The right to receive a share of production revenue

- Leasing rights – The right to lease minerals for exploration and development

- Right of ingress/egress – The right to access the surface to develop minerals (often tied to executive rights)

-

For example, one person might own the executive rights and get to negotiate leases, while another person owns the royalty interest and gets the revenue.

It all started unified—but rarely stays that way.

Originally, one person (or family) likely owned 100% of the minerals and all associated rights. But over time, through sales, inheritance, and deals with investors or developers, those rights are often “sliced and diced” across multiple parties.

That's why understanding what's being conveyed or reserved—and what's already been separated—is essential before buying or selling mineral interests.

What does it mean to transfer 20% of mineral rights?

On the surface, “20% of mineral rights” sounds simple—but in legal terms, it can mean very different things depending on how the deed is worded and what the seller actually owns.

The language matters—a lot.

Let's say you own 20% of the mineral estate under a property. Now:

-

-

- If your deed says you're selling “20% of the minerals,” that's 20% of the whole mineral estate—and you're likely selling everything you own.

- But if your deed says you're selling “20% of my mineral rights,” then you're only conveying 20% of your 20%—or — or just 4% of the total mineral estate.

-

That difference may sound minor, but in oil and gas law, that nuance is everything. This is why title attorneys and landmen read every deed word-for-word to see what was actually granted or reserved.

Why this gets complicated:

Mineral interests are often fractional to begin with, and owners may not always know exactly what they own. That's why vague or inconsistent deed language can lead to confusion—and lawsuits.

One famous legal doctrine that comes into play is the Duhig Rule (from Duhig v. Peavy-Moore Lumber Co., 1940). This case established a key principle in Texas (and followed in many other jurisdictions):

If a deed conveys more interest than the grantor actually owns, and it also attempts to reserve an interest, the reservation fails to the extent necessary to fulfill the grant.

In plain English: if you say you're selling 1/2 of the minerals and reserving 1/2—but you only own 1/2 to begin with—then you just sold the full 1/2 and didn't successfully keep anything.

Other key points in fractional mineral transfers:

-

-

- Single leases usually cover 100% of the mineral estate, even when there are many fractional owners. The operator will then pay royalties in proportion to each person's ownership.

- Each mineral owner signs separately (or is force pooled in some states), but there's no need for 10 different leases—just one lease that covers 100%, with royalties split accordingly.

- Executive rights and royalties can also be divided. You might transfer part of your mineral interest but retain the right to lease or receive bonus payments.

-

Bottom line:

Never assume a percentage is simple. “20% of the minerals,” “20% of my minerals,” and “an undivided 1/5 mineral interest” may all lead to different legal outcomes. That's why careful deed drafting—and reading prior deeds in the chain of title—is critical.

If I buy land but not the minerals, can someone access my property to drill? What rights does the mineral owner have over the surface?

Yes. In most states, the mineral estate is dominant, meaning the mineral owner (or their lessee) has the legal right to access the surface to extract minerals — even without the surface owner's permission. This includes building roads, pads, tanks, and pipelines.

Operators are limited to “reasonable use” of the surface and must minimize unnecessary damage. If they exceed that, they can be held liable for damages.

Surface Use Agreements (SUAs)

Though not always required, operators typically negotiate a Surface Use Agreement (SUA) with the surface owner. This outlines:

-

-

- Where drilling and roads can go

- Compensation for surface damages

- Restoration terms after operations end

-

If no SUA is signed, the operator can proceed but must pay damages, often resolved through state law or litigation.

State-by-state differences:

-

-

- Texas: Mineral rights are dominant, but the Accommodation Doctrine may protect certain surface uses.

- North Dakota and Oklahoma: Require statutory surface damage payments if no SUA is in place.

- Colorado: Requires pre-drilling consultation and formal surface use planning.

-

Long-Term Impact

Operators must restore the land after drilling ends, but that could be decades away. Wells often stay active for 30–50 years. The surface owner cannot prohibit access, but can seek damages or negotiate protections upfront.

What happens if a dissolved LLC reserved mineral rights?

The mineral rights don't disappear — they're still owned by the dissolved LLC or its successors. Ownership doesn't automatically revert to the surface owner unless state law provides for abandonment, which is rare and usually requires formal notice and statutory procedures.

When an LLC dissolves, its assets — including mineral rights — become part of the wind-down process. These assets are typically distributed to:

-

-

- The members of the LLC (like shareholders in a corporation), or

- Creditors, if debts are owed.

-

However, if the dissolution wasn't handled properly or no transfer was recorded in the county clerk's records, the minerals may still show as owned by the defunct entity in title.

How to find out who owns the interest now:

-

-

- Search the Secretary of State's records – Most states maintain LLC filings and list the registered agent and members. Start here to identify the people or companies behind the dissolved entity.

- Check dissolution filings – If the LLC was properly dissolved, there may be documentation showing who received the assets.

- Review probate or court records – In some cases, assets transfer through probate or legal action if the LLC's members are deceased or inactive.

- Quiet title action – If no one steps forward and the chain of title is unresolved, a surface owner (or buyer) may need to file a quiet title suit to clean up ownership—especially if the mineral rights are causing issues with a sale or lease.

-

Does zoning (residential vs. commercial) affect mineral right concerns?

Zoning doesn't change mineral ownership or dominance—the mineral estate is still legally dominant whether the surface is zoned residential, commercial, or rural. However, zoning does impact how and where development occurs.

In residential areas, mineral development faces more regulatory scrutiny, stricter permitting, and greater pushback from homeowners. Still, if the minerals weren't previously reserved, the mineral owner (or lessee) retains the right to develop.

A good example is the Barnett Shale in Fort Worth, Texas, where Landmen went door-to-door signing leases in neighborhoods. As a result, there are producing wells throughout suburban areas—often located on small pads tucked between homes, churches, and schools.

Commercial tracts face similar issues. If a company or investor owns the minerals under a shopping center, office park, or warehouse, they still retain the right to access those minerals—even if it's inconvenient for the surface owner.

The bottom line is, zoning affects how easily mineral development can occur, but it doesn't override the mineral owner's legal rights.

Can mineral rights be purchased back after severance?

Yes—but only if the current mineral owner agrees to sell. Mineral rights are real property and follow a separate chain of title from the surface. So, if you own the surface and want to “buy back” the minerals, you'll need to run title to identify who owns them, then contact those parties to negotiate.

Because mineral interests are often fractionalized, you may have to deal with multiple owners, execute purchase agreements, conduct due diligence, and close like any other real estate transaction.

Before buying, it's critical to assess the value of future production based on location, geology, and market trends—or have a buyer already lined up so you can arbitrage the spread between what you pay and what they're willing to pay.

Where do surface rights end and mineral rights begin?

There's no universal depth where surface rights stop and mineral rights begin—the division is legal, not geological, and it depends on how rights were originally conveyed or severed in the chain of title.

Here's how it generally breaks down:

-

-

- Water rights (including groundwater) usually belong to the surface owner, but laws vary by state. In many cases, landowners can drill wells and use water beneath their property—subject to local regulation.

- Gravel, sand, caliche, and limestone are often considered part of the surface estate—especially if they're near the surface and commonly used for on-site construction or development. However, they can be treated as minerals in some states or under specific contracts.

- Oil, gas, coal, and hard rock minerals (like gold, copper, lithium) are nearly always part of the mineral estate and are severed from the surface when mineral rights are conveyed or reserved.

-

So how do you know where the line is? It comes down to:

-

-

- The deed language. Some deeds specifically list which resources are being reserved or conveyed—and that's the best place to start.

- State law and precedent. Courts in different states interpret things like limestone or sand differently. In Texas, for example, limestone is often considered part of the surface estate, while oil and gas are unquestionably part of the mineral estate.

- Economic use. In legal disputes, courts sometimes consider whether the material is being used in a way that resembles mineral production. For example, if a company is commercially mining gravel and selling it off-site, a court may treat it as a mineral interest—even if it's shallow.

-

When minerals are severed:

If the mineral estate has been severed from the surface, the mineral owner may claim ownership of any resource legally considered a “mineral” under state law — even if it's close to the surface. But many shallow materials (like sand and gravel) still “go with” the surface unless expressly included in the mineral deed.

Are wind/solar rights treated like mineral rights?

No—wind and solar rights are part of the surface estate, not the mineral estate. But they can conflict with mineral development.

In places like West Texas, where both oil production and solar development are common, surface use must be coordinated. Since the mineral estate is dominant, a surface owner cannot block access to the minerals—even if a solar array is installed.

To avoid conflict, solar developers often seek surface use waivers from mineral owners or lessees. This waiver gives up the right to use the surface for oil and gas operations. It's typically negotiated with compensation, especially if the minerals are leased and held by production.

Mineral Rights Q&A: Fracking, Geology, and Drilling

How does fracking work, and how does that complicate mineral rights?

Fracking, or hydraulic fracturing, involves injecting high-pressure fluid into underground rock formations to create cracks and release trapped oil or gas. It is a key technology in unlocking unconventional reservoirs—formations that were traditionally too tight or impermeable to produce from economically.

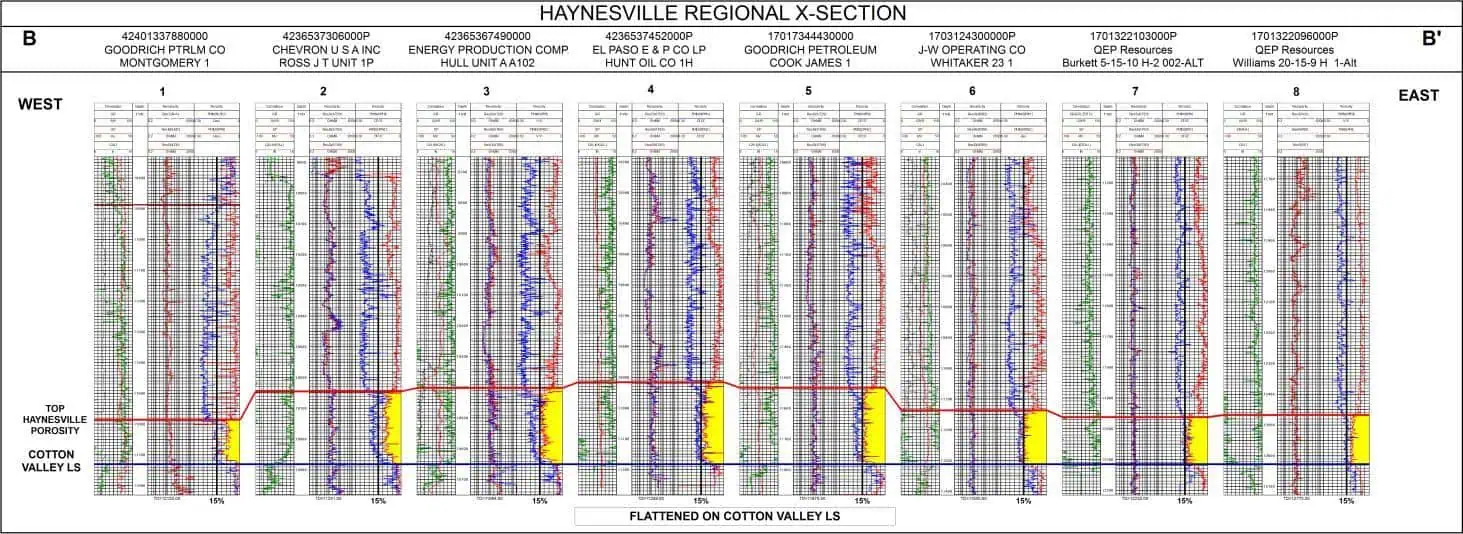

Historically, oil and gas development relied on conventional reservoirs, where hydrocarbons migrated from a source rock into porous sandstone or limestone formations. These were typically produced using vertical wells. However, with advancements in drilling technology, operators now drill horizontally into the source rock itself—typically shale—which holds vast amounts of hydrocarbons but has extremely low permeability.

Horizontal drilling allows a single wellbore to access thousands of feet of pay zone, and when combined with fracking, it dramatically increases production from these unconventional plays.

This shift complicates mineral rights because horizontal wells often cross multiple tracts, making it essential to have clear pooling agreements. A well pad on a neighboring tract might legally extract hydrocarbons from under your property—if you're within the unit and properly leased. That's why clear unitization, lease boundaries, and division of interest calculations are critical in horizontal development.

Is it ever not a speculative play to buy mineral rights?

Yes—when buying producing minerals with current cash flow or acreage permitted for imminent drilling. Buying proven producing reserves is more investment than speculation.

Reserve classifications help define this distinction. The most reliable category is PDP (Proved Developed Producing), which refers to wells that are actively producing hydrocarbons. These reserves carry the least risk, as engineers can model remaining volumes using historical production data and decline curves.

Other categories include:

-

-

- PDNP (Proved Developed Non-Producing): Reserves behind pipe or in shut-in wells that have already been drilled but aren't yet producing.

- PUD (Proved Undeveloped): Locations where reserves are known to exist and can be recovered with existing technology, but a well still needs to be drilled. These carry more risk and delay.

- PROB (Probable): Reserves likely to exist based on nearby data, but less certainty in volume or commercial viability.

- POSS (Possible): Highly speculative reserves with the least supporting data—the riskiest classification.

-

When valuing mineral rights, professionals discount each reserve category based on risk. PDP is most valuable due to cash flow certainty. PUD, PROB, and POSS are assigned lower present values due to development risk, commodity price volatility, and timeline uncertainty.

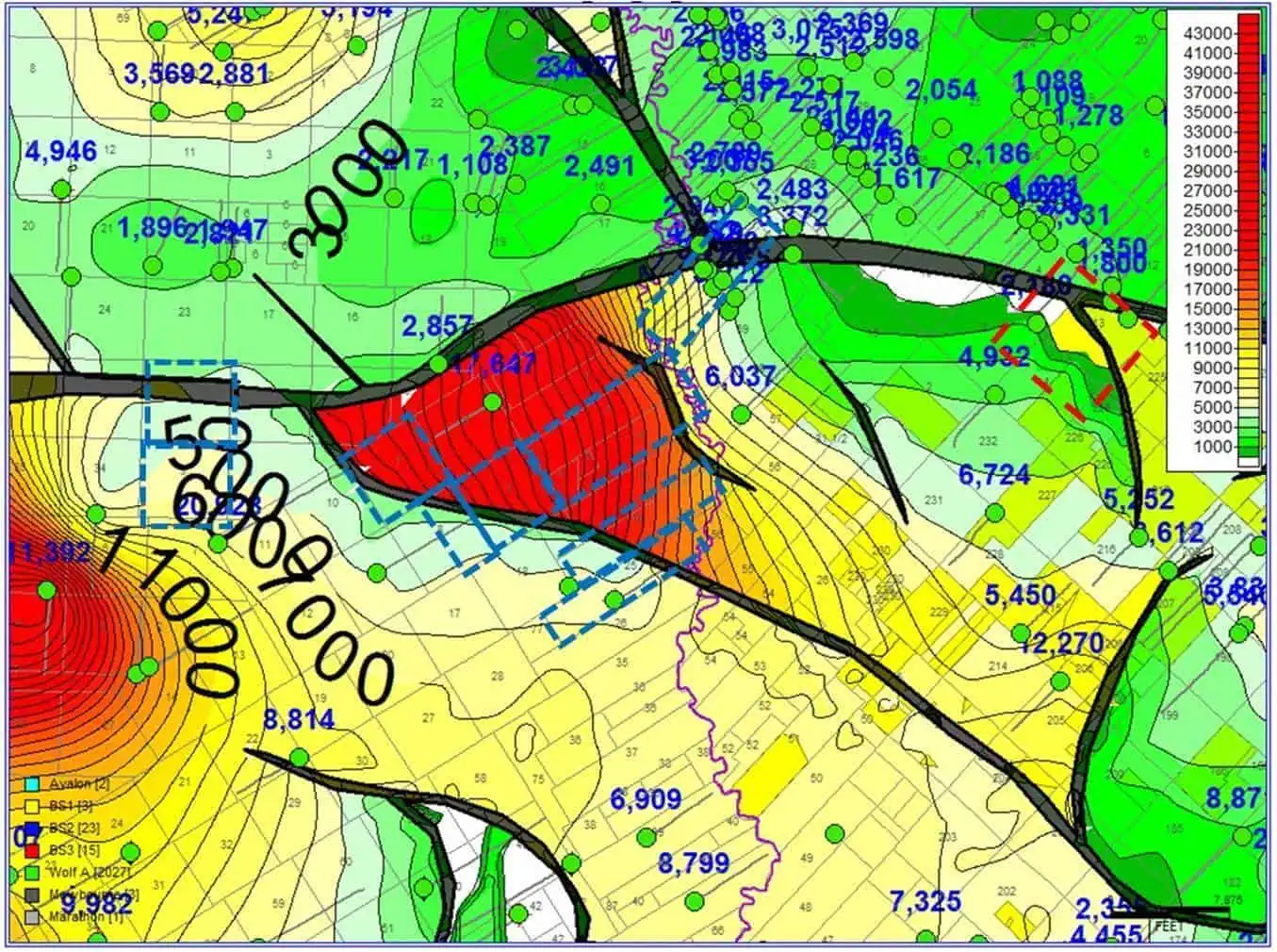

In mature, uniform basins like the Midland Basin, Delaware Basin, or Bakken, even PUD reserves carry relatively low geologic risk. In such areas, the bigger variables are timing and oil/gas prices. Mineral buyers in these regions often purchase rights at a discount to projected future income, assuming risk in exchange for upside potential.

How does the sonar/seismic thing work?

What you're referring to is called a seismic survey, and it's one of the most important tools geologists use to find oil and gas underground—before drilling.

Seismic doesn't work exactly like sonar, but it's similar in concept. Here's how it works:

-

-

- Sound waves are sent into the ground using controlled energy sources like small explosive charges or vibrating equipment (called vibroseis trucks).

- These waves bounce off layers of rock underground, and receivers (geophones) at the surface pick up how long it takes for those waves to reflect back.

- Using thousands (or millions) of data points, computers process the timing and strength of these wave reflections to create a 3D model of the subsurface geology.

-

This is critical for exploration because it:

-

-

- Helps identify geologic structures like faults, folds, and trapped layers—which might hold oil and gas.

- Lets geologists map the likely size, shape, and depth of reservoirs.

- Dramatically reduces drilling risk—especially when wells cost $5–10 million or more each.

-

Think about it this way: oil companies don't just poke random holes in the ground and hope for the best. That would be wildly expensive and inefficient. Seismic data allows them to target the highest-probability areas and avoid wasting money on dry holes.

That said, seismic data doesn't tell you exactly what's down there. It shows structures that look like they could contain hydrocarbons—but it won't say how much oil or gas is actually present or how well it will flow. It's a probability tool, not a guarantee.

So in summary:

-

-

- Seismic helps find the “where”—where to drill

- It helps de-risk exploration

- And it saves millions by avoiding bad wells

-

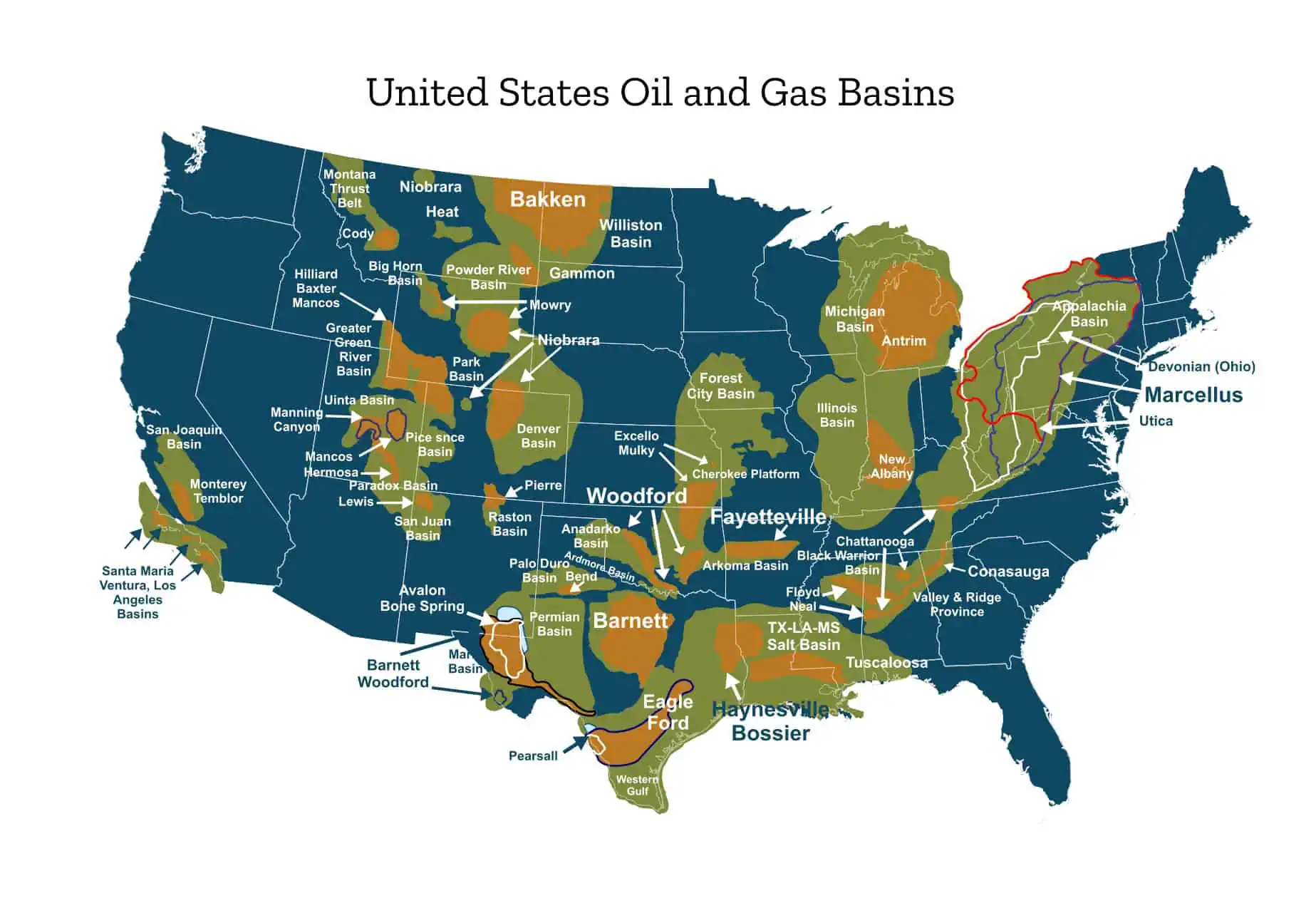

Which minerals are people most concerned with?

In most parts of the U.S., when people refer to “mineral rights,” they're typically talking about oil and gas rights—and those are by far the most commonly leased and developed mineral interests today.

But that's just one piece of the picture.

Across the country, depending on geology, demand, and technological advancement, there are many other types of valuable minerals, including:

-

-

- Coal and lignite (especially in the Midwest and Appalachia)

- Hard rock minerals like gold, silver, copper, and zinc

- Industrial minerals such as limestone, sand, and gravel (used for construction)

- Rare earth elements (used in electronics, magnets, and military equipment)

- Lithium (increasingly valuable due to demand for lithium-ion batteries in electric vehicles and energy storage)

-

The key is location and geology. Each region of the country has its own geologic profile. For example:

-

-

- Oil and gas dominate in the Permian Basin (TX/NM), Bakken Shale (ND/MT), Marcellus Shale (PA/WV), and Eagle Ford (TX).

- Lithium is being explored in the Clayton Valley of Nevada and parts of Arkansas.

- Coal and lignite are prominent in Wyoming's Powder River Basin and parts of North Dakota and Texas.

- Rare earth minerals are being explored in areas of Utah, Wyoming, and California.

-

As technology improves and the economics of extraction change, previously uneconomic resources may become viable. What wasn't worth drilling or mining 10 years ago may now be highly profitable—especially as new industries (like electric vehicles and green tech) create fresh demand for different minerals.

For landowners:

-

-

- It's important to understand what natural resources are typically found in your region.

- Check your state's geologic or mineral resource maps.

- Look at historical records to see if any minerals were previously explored, mined, or drilled on your land or nearby.

- Consider using a platform like LandGate or reaching out to a geologist or land professional if you suspect your property may have untapped potential.

-

Even if your property isn't currently leased or producing, it may still carry mineral value based on its location, geology, and surrounding activity.

Are there states where mineral rights don't have value?

Yes—mineral rights only have value if the subsurface contains something that can realistically be extracted and sold for a profit. That depends on a combination of geology, location, market demand, and technology.

While oil and gas rights are highly valuable in certain regions (like Texas, Oklahoma, and North Dakota), there are many parts of the country where mineral rights currently hold little to no value, especially for oil and gas. This is common in parts of the Upper Midwest, the Northeast, and certain interior regions where no proven productive formations exist.

But the reality is more nuanced than just “state by state”—in fact, it's often county by county, or even section by section within a county.

Key factors that impact value:

-

-

- Geologic formations don't follow county or state lines. Subsurface rocks were formed over millions of years, long before property boundaries existed. As a result, one part of a county might sit on a highly productive shale layer, while the next section over has no reservoir rock at all.

- Value is based on future productive potential. If no drilling or mining is happening nearby—and no one's leasing—the market is telling you there's likely little value there at this time.

- Technology and economics matter. Even if there is some resource underground, it might be too deep, too tight, or too dispersed to be extracted economically with current technology. That can change over time, as we've seen with shale development and rare earth elements.

-

That said, some areas that don't have oil or gas potential may still have value in other ways:

-

-

- Aggregates like gravel, sand, or limestone

- Hard rock mining (gold, copper, lithium, etc.)

- Coal or lignite (though in decline in many regions)

- Carbon credit leasing or geothermal potential

-

The bottom line is large swaths of the U.S. have mineral rights with little to no current market value. But that's not always permanent. Value is driven by geologic potential, operator interest, commodity prices, and technological advancements. Even in non-producing areas today, certain minerals could become valuable in the future.

Mineral Rights Q&A: Valuation and Investment

How do you appraise the value of mineral rights?

Valuing mineral rights requires a combination of financial modeling, comparable sales, and geologic analysis. The main approaches include:

- Income approach: This is based on the discounted cash flow (DCF) of projected royalty income. For example, if an operator drills a well expected to produce 500,000 barrels of oil over its life, and you own a 1/8 royalty interest (12.5%), your share would be 62,500 barrels. At a $70 oil price, that equals $4,375,000 in gross royalty revenue. Applying a discount rate of 15% over the projected decline curve allows investors to calculate the net present value (NPV) of those future royalties in today's dollars—possibly closer to $2.5–$3.2 million depending on timing and risk profile.

- Reserve categories and risk discounting: These future revenues are weighted based on their classification:

-

-

- PDP (Proved Developed Producing): Low risk; already producing. Discounted at 8–12%.

- PDNP (Proved Developed Non-Producing): Behind-pipe or shut-in wells. Slightly more risk at 12-15%.

- PUD (Proved Undeveloped): Drillable but not yet drilled. Discounted at 20–25%.

- PROB (Probable): Less certain than PUDs; may depend on spacing or market conditions. Discounted at 25–40%.

- POSS (Possible): High risk, highly speculative. Often discounted heavily or excluded.

-

- Geological potential: Investors evaluate whether the minerals lie within a known productive basin—like the Midland Basin, Bakken, or Delaware—where formations are continuous and well understood. In these areas, much of the risk is reduced to timing and commodity pricing rather than geological uncertainty.

- Market comps: Recent comparable sales offer insight into current market sentiment. These are typically expressed in dollars per net mineral acre (NMA). In active areas, PDP-heavy tracts may sell for $15,000–$30,000/NMA, while undrilled, speculative tracts trade for significantly less depending on location and operator activity.

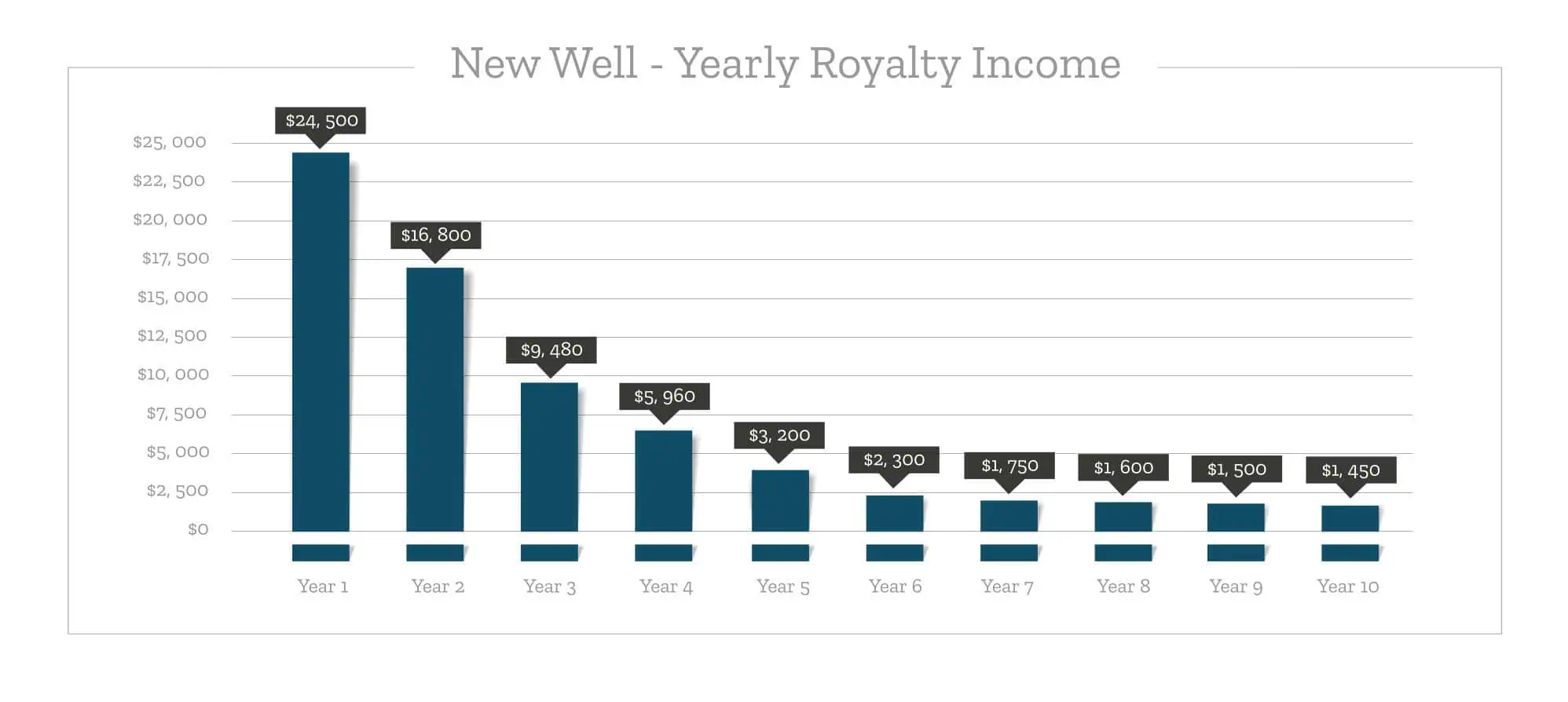

What if you buy mineral rights, and the well runs dry the next day?

That's one of the core risks of buying mineral rights—and it's why valuation must be based on future cash flow, not just current production. When you buy mineral rights tied to a producing well, what you're really buying is a share of the revenue that well will (hopefully) generate going forward. If that well stops producing, your income stream can disappear overnight.

Here's why that happens and what to understand:

- Wells decline over time. Every well has a production curve—it typically produces a lot early on and then declines, sometimes sharply. This is called a decline curve, and it’s a key tool used to model future production.

- Equipment and economics matter. Older wells use aging equipment, and production costs often rise over time. If the expected remaining oil or gas isn’t valuable enough to cover the cost of getting it out of the ground, the operator might shut the well in (temporarily) or plug it (permanently abandon it).

- Reserve life is limited. Engineers can usually estimate how much recoverable resource remains based on production data. If a well doesn’t have enough “life” left to justify maintenance or rework, it will likely be shut-in or plugged.

- Mineral owners don’t control the operator. As a mineral rights owner, you aren’t in charge of operations—the oil or gas company is. That means they decide whether to reinvest in the well, sell to another operator, shut it in, or drill another one nearby. However, staying in touch with the operator (or checking public records) can help you understand their development plans.

- Know what you’re buying. Before buying mineral rights, especially in a producing area, try to review:

- Well history: When was it drilled? What’s its production trend?

- Operator behavior: Are they active in the area?

- Remaining reserves: How much oil or gas is likely left?

- Offset drilling: Are other wells being drilled nearby?

Bottom line: if you buy into a well late in its life and it gets shut in right after, you may have overpaid. That's why smart mineral buyers use decline curves, production history, and economic modeling to estimate future revenue—and apply a discount to reflect the risk that things don't go as planned.

Could a lack of mineral rights hurt my resale value?

Yes—especially with informed buyers in actively explored areas of oil and gas, coal and other minerals.

That said, value depends on market context. If you're buying and the seller doesn't assign value to the minerals, you're not really paying for them. If the property is in an area with no known production, there might be very little if any value.

But if you're selling in a known oil and gas area and you own mineral rights, it makes sense to separate the value of the surface from the minerals—since the minerals may represent future revenue from leasing, royalties, or production.

Smart sellers in producing regions often reserve the minerals or negotiate a separate sale, especially when there's clear geologic and operator interest.

Is there a marketplace for buying/selling mineral rights?

Yes. Examples: EnergyNet, LandGate, MineralWare, US Mineral Exchange, Energy Domain, direct mail offers, brokers, and auction platforms. Private equity also actively buys minerals.

How do you evaluate mineral rights as an investment?

Estimate potential:

- Royalty % and lease terms

- Likelihood of leasing

- Drilling permits nearby

- Historical production Then model projected cash flows, apply a discount rate (often 10–25%), and compare to purchase price.

Mineral Rights Q&A: Leasing and Royalties

How big of a concern is it when mineral rights are reserved?

If there's no current mineral development in the area, it may be a minor concern. In active basins, it can affect land use, development, and property value. Always check to see what kinds of activity have historically occurred around your area.

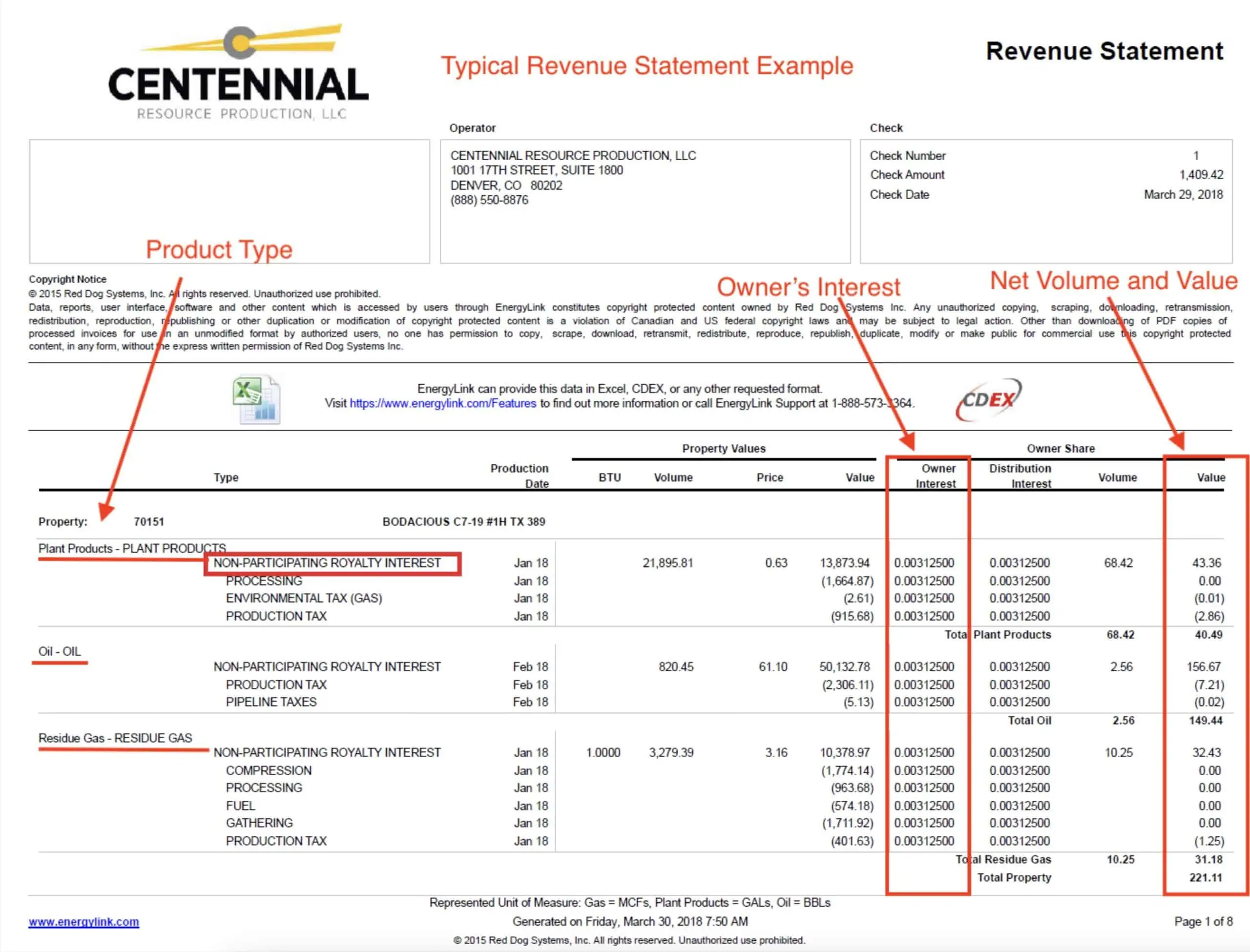

How do I calculate how much my royalty should be? (Understanding Division of Interest)

Your royalty check is based on your Division of Interest (DOI)—which represents the fraction of total production you're entitled to from a well or unit. To calculate this, you need to know:

- How many net mineral acres (NMA) you own

- The size of the unit the well is drilled in

- The lease royalty rate (typically between 12.5% and 25%)

Example scenario:

You own 50% of the minerals under a 20-acre tract, and that tract is part of a 640-acre pooled unit. You signed a lease with a 20% royalty.

Step-by-step calculation:

- Calculate your Net Mineral Acres (NMA). You own 50% of the 20-acre tract: 20 acres × 0.50 = 10 NMA

- Divide your NMA by the total unit size. You are part of a 640-acre pooled unit: 10 NMA ÷ 640 acres = 0.015625

- Multiply by your lease royalty rate. You signed a lease at 20% (0.20): 0.015625 × 0.20 = 0.003125

Final result:

Your Division of Interest (DOI) is 0.003125. That means you would receive 0.3125% of the revenue from that well's production.

So if the operator sells $1,000,000 of oil and gas in a given month, your share would be: $1,000,000 × 0.003125 = $3,125

Why this matters:

Even a small DOI can add up over time, especially when prices are high or if you're part of multiple wells. Understanding this math helps you verify royalty checks and evaluate what your minerals might be worth if you choose to lease or sell.

Let me know if you want to show how multiple tracts or leases impact the calculation, or if we should move to the next question in your list.

What is a pooled unit, and how does it affect my royalty payments?

A pooled unit is a legal mechanism used in oil and gas to combine multiple tracts of land—often owned by different people—into one unit for the purpose of drilling a single well. Instead of drilling a separate well on each tract (which would be inefficient and costly), the operator drills one well and shares the production revenue proportionally among all the mineral owners in the unit.

This process is called pooling, and it's typically authorized in the oil and gas lease through a pooling clause. In some states, if not all mineral owners agree to lease, the operator can still form a unit through forced pooling with regulatory approval.

Why pooling matters:

- Protects mineral owners. Pooling ensures you get paid your share of production—even if the well isn't located directly on your tract. Revenue is divided based on how much acreage you contribute to the unit and your lease terms.

- Protects operators. It prevents legal disputes over drainage and allows operators to drill the most efficient well, often saving millions in development costs.

- Preserves the value of the reservoir. Pooling avoids drilling unnecessary or competing wells that could reduce pressure and waste the resource.

How royalties are affected:

Your Division of Interest (DOI) is calculated using this formula: (Net Mineral Acres ÷ Unit Size) × Royalty Rate

For example, if you own 10 net mineral acres in a 640-acre unit with a 20% royalty: (10 ÷ 640) × 0.20 = 0.003125 or 0.3125%

That's your share of all revenue from the well in the pooled unit.

Mineral Rights Q&A: Legal Issues and Regulations

Who regulates mineral rights at the state level?

Mineral rights are considered real property, and their ownership is governed by state property laws and decades of court precedent. These legal frameworks evolve over time as new cases test old interpretations—especially around conveyance, severance, and title disputes.

Meanwhile, exploration and production activities, such as drilling, pooling, permitting, and surface impact, are typically regulated by a state agency. For example:

- Texas: Texas Railroad Commission (RRC)

- North Dakota: Industrial Commission

- Colorado: Colorado Energy & Carbon Management Commission (ECMC)

There's often interplay between the courts and agencies. Here's how it typically breaks down:

- Handled by courts/legal precedent:

- Who owns what (title disputes)

- Mineral vs. surface rights interpretation

- Deed language and reservations

- Executive rights and royalty claims

- Handled by state regulatory agencies:

- Well spacing and permitting

- Forced pooling rules

- Surface use and environmental compliance

- Flaring, production reporting, and abandonment

A mineral owner might end up in both systems: leasing or pooling disputes may go through the agency, while ownership or revenue share disagreements are resolved in court.

How does a surface use agreement work?

A Surface Use Agreement (SUA) is a private contract between the surface owner and the mineral rights holder (or their lessee). It outlines how the operator can access and use the land to drill for minerals.

Typical terms include:

- Ingress and egress access points

- Pad site and road placement

- Payment for surface damages

- Cleanliness and maintenance obligations

- Restoration requirements after operations are complete

While the mineral estate is dominant, SUAs help clarify rights, avoid disputes, and ensure fair compensation to the surface owner.

What's the difference between surface rights, mineral rights, royalty interests, and other types of ownership?

Think of the fee simple estate (full ownership of land) as a bundle of sticks—each stick represents a different right that can be separated, conveyed, or retained. Over time, these rights are often split among different parties. Here's how the key components break down:

- Surface rights – The right to use and occupy the surface of the land (e.g., farming, building, access). Does not include subsurface rights unless specifically retained.

- Mineral rights – Ownership of the subsurface minerals (oil, gas, etc.) and the right to explore, drill, and produce—or lease those rights to someone else.

- Executive rights – The authority to negotiate and sign oil and gas leases on behalf of all or part of the mineral interest.

- Royalty interest – The right to receive a share of production revenue, without bearing drilling or operating costs. Usually expressed as a percentage of production.

- Non-participating royalty interest (NPRI) – A royalty interest that does not include executive rights. The holder gets paid royalties but cannot negotiate or sign leases.

Each of these can be split off and sold or inherited separately. That's why clear title and deed language are critical in mineral transactions.

If I own surface but no minerals, do I get compensated for drilling?

Not directly. You may be compensated for surface damages, but not royalties unless negotiated separately.

How are lease offers handled when multiple people own the same minerals?

When multiple people own undivided interests in the same mineral tract, each person owns a percentage of the entire property, not a specific section. As a result, each owner has the right to negotiate and sign their own lease with the operator.

In some cases, family members or co-owners choose to negotiate jointly under a single lease. But more commonly, each owner signs a separate lease, often with different terms. An owner with a larger interest—or one strategically located within a planned drill site—may have more leverage to negotiate for a higher royalty, better surface protections, or operational restrictions.

If most owners lease and a few hold out, forced pooling laws in some states (like Oklahoma and North Dakota) allow the operator to pool those unleased interests under regulatory oversight.

Can mineral rights be abandoned from non-use?

In some states, yes—but it's rare. A few states have Dormant Mineral Acts that allow surface owners to reclaim severed mineral interests after a long period of non-use.

For example, Louisiana has a “prescription of nonuse” rule: if mineral rights aren't used (e.g., leased, produced, or explored) for 10 years, they automatically revert to the surface owner unless action is taken to preserve them.

Other states like North Dakota, Ohio, and Indiana have Dormant Mineral statutes, but the process isn't automatic. Surface owners must file affidavits or court actions and give notice to the mineral owners or heirs. If no response is made, the minerals may be cleared and transferred.

These laws vary widely in terms of timing, process, and enforceability, and they're not recognized in most major producing states like Texas or Oklahoma.

Can buyers find surprise encumbrances after closing?

Yes—it's common to discover unrecorded leases, outdated production still holding a lease, fractional interests passed through generations, or prior conveyances that weren't properly documented. These issues can cloud title, delay leasing, or reduce your actual interest. To avoid this, conduct a full mineral title review, not just surface title—ideally with a landman or title attorney familiar with oil and gas.

What due diligence steps should I take in mineral-rich areas?

If you're buying property in an oil- and gas-producing area—and you're unsure whether mineral rights are included—follow this plan:

- Start with the title company. Ask if they can recommend a title abstractor to pull a full chain of title for the mineral estate. This will help you see if any prior owners reserved or conveyed mineral rights.

- Hire a landman. A qualified landman can prepare a Mineral Ownership Report (MOR), showing what mineral interest, if any, is still attached to the property.

- Check for leases and production. If the minerals are leased and currently producing, the lease may be held by production (HBP). Ask the seller if they're receiving royalties — this should come up during negotiations.

- Verify royalty status. Contact the owner relations department of the operator listed on nearby wells. Ask if they're paying royalties on the tract and request confirmation of ownership.

- Review royalty statements. If the seller is receiving royalties, request a recent paystub. It will show their division of interest and monthly payments. This helps you estimate current and future value.

- Assess future upside. Use public drilling records or consult a local landman to evaluate whether additional wells are likely. This can significantly impact value.

This process helps you avoid surprises and determine whether the mineral interest is worth pursuing—or if you're just buying the surface.

Are there protections against destructive extraction if I don't own minerals?

Some protections exist, but they vary by state. Many states require operators to negotiate a Surface Use Agreement (SUA) or pay surface damages. However, if you purchase land after an SUA is already in place, you'll be bound by the terms your seller agreed to.

Operators must generally confine activity to a defined surface pad, and while drilling can be noisy and disruptive, most of the mess stays within the pad boundaries. Urban areas often have stricter zoning, setbacks, and permitting requirements, but none of this overrides the fact that mineral owners retain the right to develop their resources.

If no SUA exists, you still have the right to reasonable use protections and may seek compensation for excessive damages—but enforcement usually requires legal action.

What should be in a lease to protect the landowner?

If you own both the surface and mineral rights, you have more leverage to negotiate lease terms that protect your land and prevent long-term encumbrances. Key provisions to include:

- Surface Use Restrictions – Limit where roads, pads, and equipment can go. Require fencing, noise control, and site restoration.

- Pugh Clause – Ensures only producing acreage is held by the lease, releasing any undeveloped portions after the primary term.

- Royalty Clause – Specify royalty percentage and restrict or prohibit post-production deductions.

- Shut-in Clause – Requires timely shut-in payments if a well is not producing, and sets limits on how long the lease can be held without activity.

- No Assignment Without Consent – Allows you to approve or deny lease transfers to third parties.

- Depth Severance Clause – Releases deeper or shallower zones that are not drilled.

- Many other clauses are needed to properly construct an oil and gas lease. It is recommended you work with a knowledgeable oil and gas attorney to help you with ensuring you have a well negotiated lease that protects you as the mineral owner, as well as protect the surface estate.

If the operator wants to drill on your property, you'll also want to negotiate a separate Surface Use Agreement (SUA) to cover compensation, site layout, and surface restoration.

Should I get title insurance covering minerals?

Most title insurance policies exclude mineral rights. If you want to verify mineral ownership, the standard approach is to hire a landman to run mineral title and produce a Mineral Ownership Report.

To take it further, you can have an oil and gas attorney issue a title opinion based on that report. While this isn't the same as title insurance, a title opinion provides a legally reviewed analysis of ownership and can be used to support your position in case of a dispute. It's the closest equivalent to title insurance in the mineral world.

Can I 1031 exchange mineral rights?

Yes—mineral rights qualify as real property for 1031 exchange purposes, as long as they're perpetual (not leasehold interests). This means you can defer capital gains taxes by exchanging mineral rights for other qualifying real estate, or vice versa. However, the properties must be “like-kind,” and the exchange must follow strict IRS timelines and procedures. Always consult a 1031-qualified intermediary and tax advisor before proceeding.

What happens to mineral rights in a tax sale or foreclosure?

It depends on how the rights are severed. If the mineral rights are separate from the surface, a tax sale of the surface typically does not include the minerals—they remain with the original mineral owner. But if the mineral rights were never severed, they may transfer with the surface unless separately protected. Always check the chain of title and any recorded severances when evaluating tax sale properties.

Share Your Thoughts

-

-

- Leave your thoughts about this episode on the REtipster forum!

- Share this episode on Facebook, X, or LinkedIn (social sharing buttons below!)

-

Help out the show!

-

-

- Leave an honest review on Apple Podcasts. Your ratings and reviews are a huge help (and we read each one)!

- Subscribe on Apple Podcasts

- Subscribe on Spotify

-

Thanks again for listening!

Great conversation! Vernon’s insights into breaking into the appraisal profession are both practical and motivating. At GoSource Valuation, we’re always eager to support new and experienced appraisers in delivering accurate, compliant valuations across the U.S.