What happens when you find a lucrative, de-risked deal with an experienced operator…and your standard deal structure is completely unusable?

We’ve been going upmarket. Nothing below $50K purchase price, $150K+ preferred. More experienced operators. Less volume, greater absolute returns.

For higher-value deals (rough guideline: anything above ~$200K to $250K purchase price)…they almost always come with greater complexity from due diligence, value-add, regulatory, and/or structuring perspectives.

(Not always, as you may occasionally find a large acreage tract or a luxury infill lot above that price that’s relatively straightforward. On the flip side, messy title deals may require enormous effort to acquire, with a lower purchase price.)

Quick Breakdown on Entitlement Deals

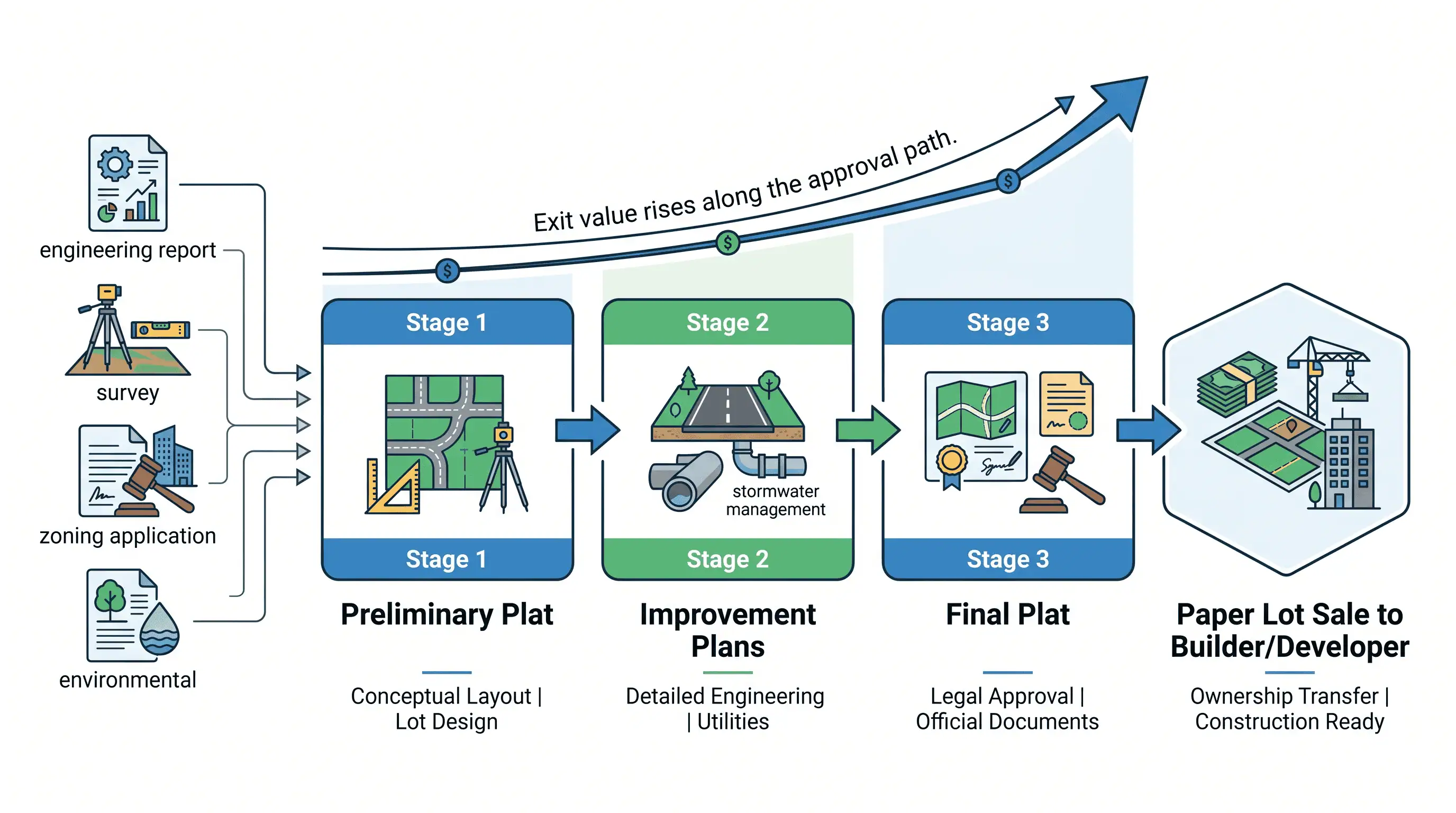

A deal type we’ve been spending a lot of time on recently is entitlement deals…specifically, funding the soft costs (e.g., engineering reports, planning and zoning applications, surveys, environmental consulting, etc.) to get major subdivide projects ready for a paper lot sale to a developer/builder at various stages (e.g., preliminary plat, improvement plans, final plat).

Generally, the exit price will be higher the further down the approval pathway, and occasionally, exits can occur before any approval is granted.

Soft costs (for the paper lot stage) might range anywhere from ~$100K to $500K on average (sometimes less, sometimes more, depending on the project). The potential upside? Low seven figures on an attractive asset in a strong location.

The critical risk here…you typically don’t own the underlying asset. You have a purchase agreement from the initial seller, you’re paying for the entitlement work, and you’re selling paper lots to the end buyer.

If the buyer pool dries up, development issues arise or costs balloon, the seller bails, and/or the local planning authority nixes your plan…your invested capital goes to zero, with no recourse.

The better version of this play (and a requirement for us to consider funding) is to have the end buyer already lined up (with a signed LOI, at minimum) before you start incurring soft costs. Reduces timeline and market risk, and gives you a much clearer picture of actual returns.

(And the absolute best version is having the end buyer fund ALL the soft costs, in addition to the EMD and land acquisition costs, while you still take a cut of the profits for facilitating the deal. That takes several years of relationship building, and I know of only one group that has pulled off this model. The vast majority of the time, you’re on the hook for at least some of the soft cost capital.)

The IRA Problem

We’ve been deep in review of some of the best entitlement deals we’ve seen sourced by the aforementioned experienced operator at the start of this newsletter, however…

One problem. A big one.

The operator’s investing entity (which already contributed capital and owned the underlying LLCs tied to contracts specific to each deal under review) was a self-directed IRA (Individual Retirement Account with self-directed investment authority), which comes with a whole list of prohibitions around the owner’s ability to personally guarantee investments or have any of their other assets cross-collateralize the IRA’s deals.

Our preferred structure? An operating loan with a limited recourse (e.g., bad actor clauses) personal guarantee.

Completely unusable in this scenario.

When Debt Becomes Worthless

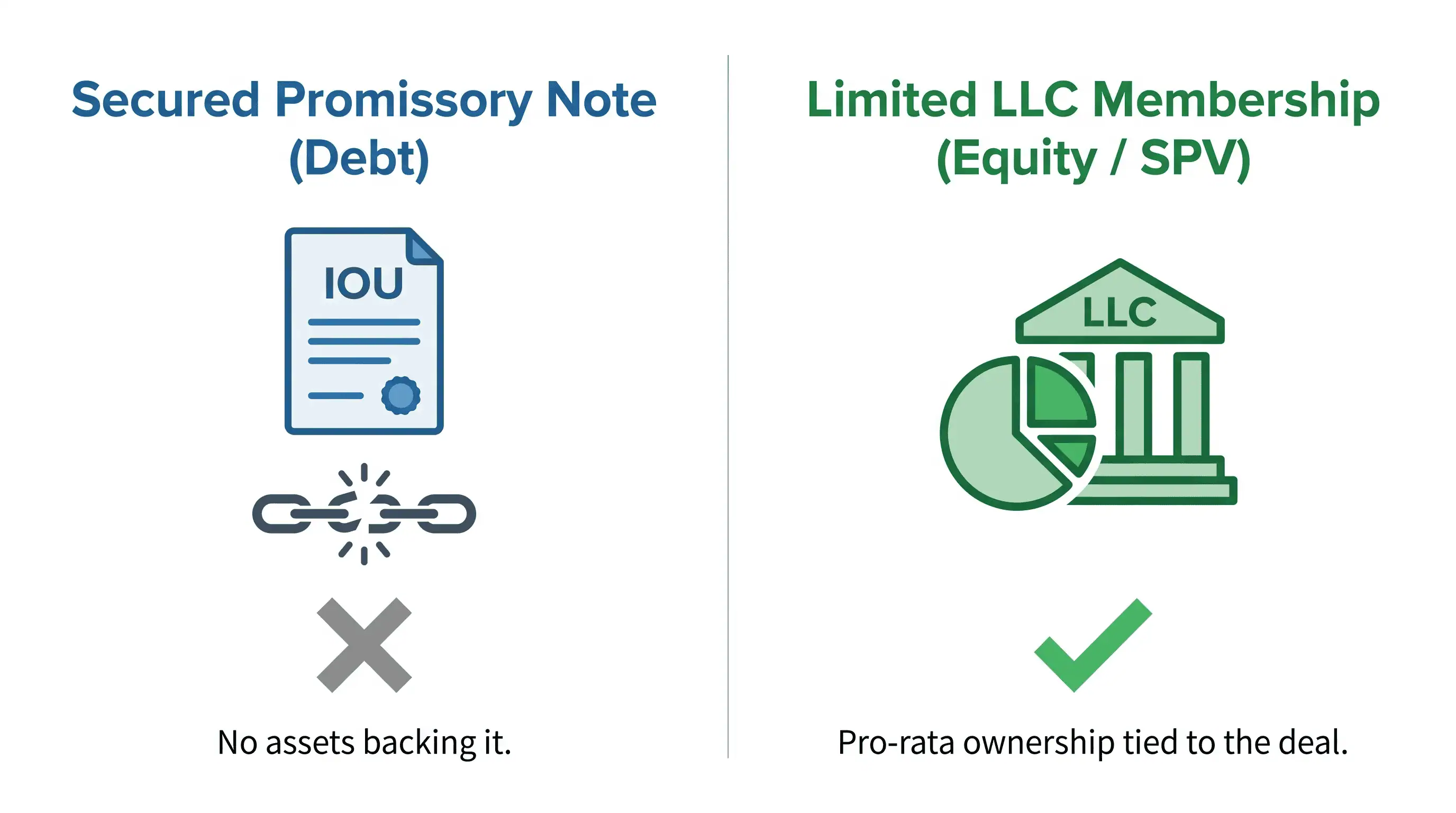

So we looked at a different debt structure, in the form of a secured promissory note.

Without the ability to cross-collateralize anything with the operator personally, the debt was effectively worthless. If the deal went south under a limited-recourse structure, there would be no underlying assets for us to pursue. The paper says we’re owed money, but there’s nothing backing it up.

And remember, even with reputable end buyers lined up and a favorable approval pathway, these are inherently higher-risk deals with significant complexity… even for limited capital amounts (in these cases, we were looking at ~$50K–$175K checks).

Rule #1 in investing (any asset class): Don’t lose money. Every dollar has to be deployed carefully and thoughtfully.

I’ll be honest…I was initially more comfortable with the revised debt approach, and I was excited that we were ‘almost home’ on a couple of strong deals in a difficult market.

But my business partner, who has spent many years working on major, complex corporate restructurings, just kept listing the reasons why the debt path and the return profile were inappropriate from a risk-management standpoint… and he was right.

(The lesson here is maybe just as important as the structural one…you’ve got to have the humility to defer to your partner’s expertise, or when conflicting data is brought to your attention, even when it means scrapping hours of work and starting over…or potentially losing out on a deal.

Sometimes, inertia is your biggest enemy. You don’t want to have to go back and rethink everything, so you rationalize the path you’re already on. The comfortable route is the lazy one. That’s a trap we humans have to remain constantly vigilant for.)

The SPV Pivot

So we thought hard about what could still make these deals work. We’ve structured investments before using an LLC framework in the form of an SPV (Special Purpose Vehicle, which is basically a standalone legal entity created specifically for a particular investment or project), allowing different investors to come in via equity and have ownership within the SPV.

Could we adapt that here?

Turns out…yes. There are no prohibitions on a self-directed IRA (that is a sole member of an LLC) from having other investors come into the LLC as members, so long as we are not personal relations of the operator behind the IRA. So, instead of debt, we structured it so that our LLC would be a limited member of the underlying operating LLC.

Although we bear the same risk of the deal falling apart and our invested capital going to zero, we have actual pro-rata ownership of the LLC, which gives us inherently greater legal protection tied to the deal we’re trying to close, compared to debt backed by no assets.

Plus, we utilized our promote structure (a performance-based incentive tier that boosts upside to the primary deal operator), similar to what we’ve done on other deals, and is heavily weighted toward the financial benefit of the operator, while still giving us an appropriate return profile for the level of risk our capital is exposed to. No personal guarantee needed. And no UCC-1 filing needed (that’s a recorded lien filed against an entity incurring debt, basically a public tracker in county records).

Cleaner. More protective. Better aligned with the actual risk profile.

The Payoff

After a couple of hours, we spent time reformatting the structure and massaging the messaging… the operator agreed to the framework.

That’s the part I’m most excited about. An experienced operator who trusts us enough to work through a completely restructured deal, and who understands that we’re (necessarily) sticklers on documentation and risk management, all in favor of building long-term, sustainable partnerships.

(Real estate is rife with freewheeling dealmakers, backing outcomes with handshakes instead of paperwork, and that will come back to bite them sooner than later…if it hasn’t already. I’ve learned that the hard way, a story for another time.)

The broader takeaway? Higher-level deals require higher-level problem-solving. AI is a massive lever (I use it extensively to think through structure and legal agreement adjustments), but it won’t rescue you if you don’t understand what the end goal should be. The context matters more than anything…and if you don’t even know what question(s) to ask, you’re going to get boilerplate nonsense back.

The willingness to do the hard work…the creative structuring, the uncomfortable back-and-forth between partners and operators, the scrapping of hours of prior effort when the situation calls for it, the capability to put aside ego (probably the HARDEST part for most entrepreneurs)…that’s where you’ll earn the returns most folks will never bother to fight for.

Need a capital partner who does the extra work on deal structuring and documentation, for long-term, mutual success? We’ve funded over $6.5M in land deals with industry-leading 41% operating margins, and we close 100% of deals we commit to. $50K+ check sizes. National underwriting experience on every transaction.

If you’re an experienced operator with a steady deal flow and you want a partner who won’t cut corners… let’s talk.

Get Your Property Analyzed Today

Originally published at SeriousLand.capital on February 16, 2026.