What Is Loan Default?

REtipster does not provide tax, investment, or financial advice. Always seek the help of a licensed financial professional before taking action.

Shortcuts

- A loan default is when a borrower stops paying debt as required by the loan’s terms.

- Financial difficulties, natural disasters, and honest mistakes are usual reasons why people are in default on their loans.

- Lenders declare a loan is in default only if the borrower has stopped making consecutive payments over a certain period, depending on the type of loan.

- A default can negatively affect one’s credit for seven years, especially if the lender collects, adding a negative item that can also stay on a credit report for seven years.

- A default is not a crime, but one could face imprisonment by not participating in the civil case accordingly.

What Causes Loan Default?

Financial difficulties (due to losing a job or getting sick) are the most common reason why a borrower defaults, especially in the context of mortgage default. Moreover, if the borrower does not have a rainy day fund[1], this only complicates or compounds the problem.

However, not all defaulting borrowers are financially irresponsible. For example, some may choose not to pay their mortgages due to negative equity, as was seen in the 2008 financial crisis[2].

College graduates often default on private and federal student loans because entry-level salaries don’t cover student loan payments. Student loan default is one of the most common examples of when a person might default.

Another culprit in loan defaults is natural disasters. For example, some homeowners’ insurance policies cover storm damage but often require a higher-than-usual deductible[3]. One might use cash intended for a loan installment to pay the deductible when caught unprepared.

Lastly, some borrowers simply forget to make a loan payment. Just missing one monthly payment can lead to a hike in interest rates and create a domino effect that eventually results in a defaulted loan. Unfortunately, honest mistake or not, the consequences for a loan default are the same.

BY THE NUMBERS: 78% of Americans have an emergency fund, but only 45% have savings adequate to cover six months’ living expenses.

Source: Fox Business

Missing Payments vs. Defaulting

Missing a payment is not necessarily defaulting. Only when a borrower misses a few consecutive payments does the lender declare the debt to have defaulted.

Lenders handle loan defaults differently depending on the kind of loan.

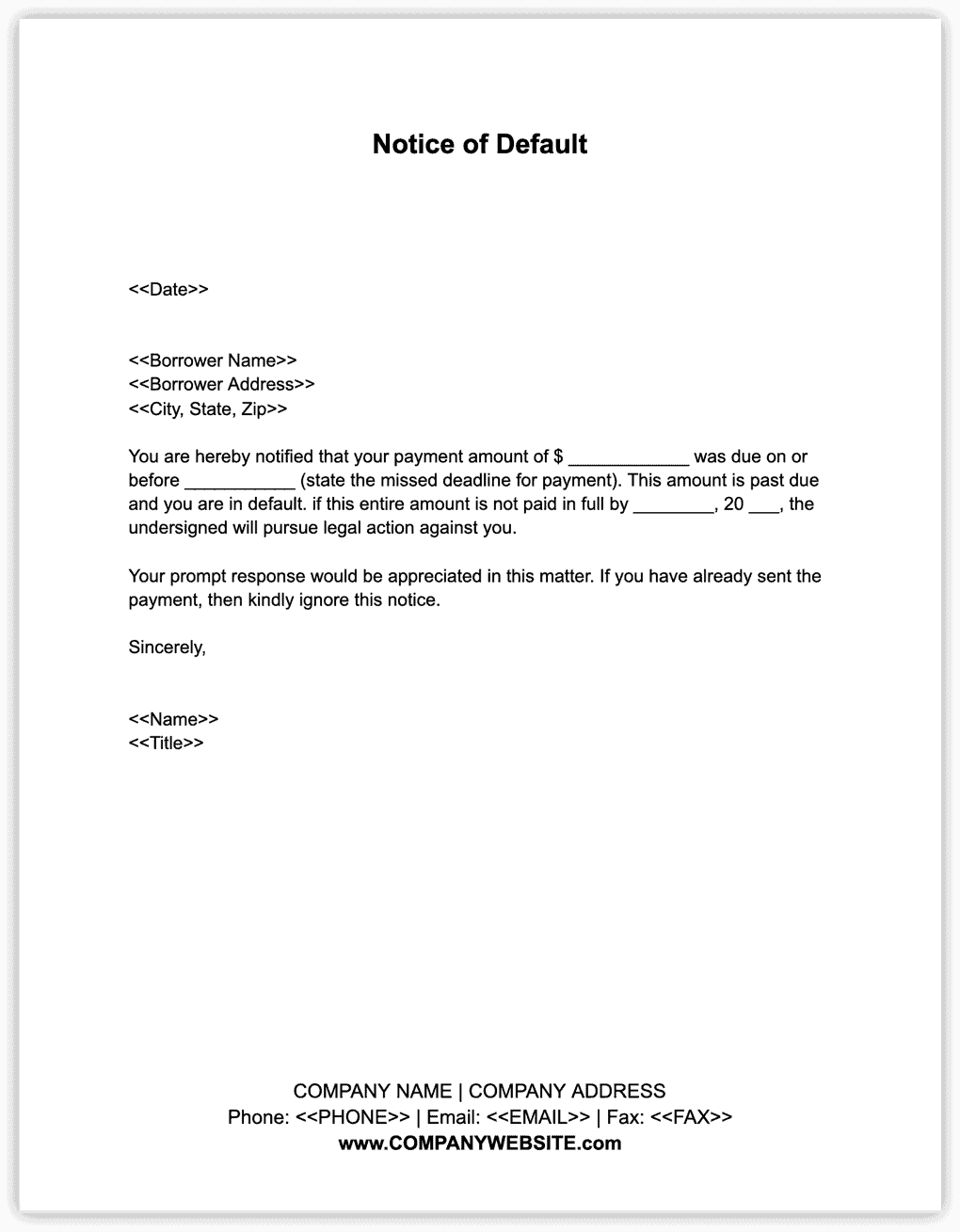

A template for a typical notice of default.

For example, missing just one mortgage payment typically results in a payment default, bringing the property one step closer to foreclosure[4]. However, most mortgage lenders only send a notice of default after three straight missed payments. The same is often true of auto, personal, and most student loans.

Upon receipt, this formal warning pressures the borrower to repay what is stated within a certain period, or the foreclosure process will proceed to the next phase[6].

While private loans have varying timelines for default, federal loans—including federal student aid—reach default status only after nine months of non-payment. Then, they may be collected through wage garnishment[7] and/or withholding of tax refunds.

Is It a Crime to Default?

Defaulting is not necessarily a crime. However, the lender may sue the delinquent borrower over the default in civil court as long as the statute of limitations has not passed.

However, ignoring a court notice stemming from a debt lawsuit may result in jail time. In addition, even if one does not recognize the plaintiff, failing to appear in court on the designated date could be grounds for a warrant of arrest.

Why Pay Off a Default

It is necessary to pay off debt obligations because defaulting on a loan can stay on one’s credit record for up to seven years. Once there is a record of payment past due by more than 30 days, the credit bureaus can knock 100 points off one’s credit score[8]. The consequences of a loan default can be much more severe.

Depending on the borrower’s bracket, this score deduction can push individuals one bracket down[9]. Such a fall may cost thousands of dollars in extra interest[10] when applying for a new loan or credit card later on.

Also, if the lender collects (i.e., selling the debt to a debt collection agency), it invariably adds a collection record on the borrower’s credit file[11]. This negative item is a record separate from the default, which remains on one’s credit reports for seven years.

Even worse, addressing a collection by paying the delinquency does not always guarantee that the borrower’s credit score goes up again. For instance, if the borrower was frequently delinquent in loan payments, paying one severely overdue debt off may not improve their creditworthiness.

Therefore, it is in the best interests of anyone who plans to take out a new loan to avoid defaulting, or at least without this blemish on their credit record.

While any loan default will hurt a person’s credit score, defaulting on secured loans can cause one to lose substantial assets. If a person secures funding by putting up their mortgaged property as collateral, a defaulted loan may result in that person having their property seized.

Sources

- Walker, B. (2022.) How a Rainy Day Fund Differs from an Emergency Fund. FinanceBuzz. Retrieved from https://financebuzz.com/rainy-day-fund

- Ohanian, L. (2017.) Who Defaults on Their Mortgage, and Why? Policy Implications for Reducing Mortgage Default. Federal Reserve Bank of Minneapolis. Retrieved from https://www.minneapolisfed.org/article/2017/who-defaults-on-their-mortgage-and-why-policy-implications-for-reducing-mortgage-default

- Hubbard, A. (2022.) Does homeowners insurance cover hurricane damage? Bankrate. Retrieved from https://www.bankrate.com/insurance/homeowners-insurance/hurricane-damage/

- Yale, A. (2021.) What Are the Stages of the Foreclosure Process? The Balance. Retrieved from https://www.thebalance.com/foreclosure-basics-1798178

- Wan, A. (2022.) Here’s How to Know When Your First Mortgage Payment Is Due After Closing. NextAdvisor with TIME. Retrieved from https://time.com/nextadvisor/mortgages/when-first-mortgage-payment-due/

- Elias, S. (2020.) Foreclosure Timeline: After You Receive a Formal Notice of Foreclosure. Nolo. Retrieved from https://www.nolo.com/legal-encyclopedia/free-books/foreclosure-book/chapter9-3.html

- U.S. Department of Labor. (n.d.) Garnishment. Retrieved from https://www.dol.gov/general/topic/wages/garnishments

- O’Shea, B. (2022.) Minimize Credit Score Damage From Late Payments. NerdWallet. Retrieved from https://www.nerdwallet.com/article/finance/late-bill-payment-reported

- DeNicola, L. (2022.) Your guide to credit score ranges. Credit Karma. Retrieved from https://www.creditkarma.com/advice/i/credit-score-ranges

- Christy Bieber, C. (2022.) How Does Your Credit Score Affect Your Mortgage Rates? The Ascent. Retrieved from https://www.fool.com/the-ascent/mortgages/how-does-credit-score-affect-mortgage-rates/

- White, J. (2020.) Will a Default Be Removed if It’s Paid? Experian. Retrieved from https://www.experian.com/blogs/ask-experian/will-a-default-be-removed-if-paid/