What Is a Performing Note?

REtipster does not provide tax, investment, or financial advice. Always seek the help of a licensed financial professional before taking action.

Shortcuts

- Performing notes are real estate notes tied to mortgage loans where the borrower is current on (i.e., they’re paying on time).

- Buying performing notes lets you invest in real estate and earn passive income without buying, owning, or managing physical properties.

- Performing notes can be a wise investment, generating steady income from mortgage borrowers who pay on time.

- Performing notes start as assets but can become liabilities if mortgage borrowers fail to keep up with payments.

- You can buy performing notes from online marketplaces, where lenders, brokers, hedge funds, and real estate investors sell them.

Investing in Performing Notes

Investing in mortgage notes can be wise as they let you grow your money in real estate without buying physical properties or dealing with related hassles[1].

Performing notes are ideal if you’re a cautious investor and want steady income. However, they’re pricier since they’re not discounted like non-performing notes.

How Do You Invest in Performing Notes?

You can invest in performing notes by buying them directly from lenders or investors through mortgage note exchanges.

Real estate lenders often deal with wholesale buyers only, while online marketplaces use retail pricing. So, banks may ignore you unless you buy in bulk, and traders may not offer big discounts.

You can also find mortgage notes from brokers and hedge funds[2]. They typically sell notes that used to be non-performing but rehabbed them to assist borrowers financially.

Downsides of Investing in Mortgage Notes

Investing in mortgage notes has some downsides.

First, you won’t benefit from its appreciation since you don’t own the actual property. Therefore, inflation may outpace your yearly earnings.

Second, if you miscalculate the property values, it can trick you into thinking that you won’t lose money if you have to foreclose to get your money back.

Third, mortgage notes can be hard to sell quickly. If you own newer or lower-quality performing notes, you may have to sell them at a significant discount.

Finally, collecting payments can hit profits. If you’re inexperienced or don’t have the time to deal with borrowers, you can hire a loan servicing company[3], but their fees will reduce your total income.

RELATED: 088: A Seamless Solution for Buying and Selling Real Estate Notes

Are Notes Assets or Liabilities?

Performing notes are considered assets as they generate income. Non-performing notes may not earn passive income, so they can be considered risky investments, but not necessarily liabilities.

However, an asset can become a liability, and vice versa. If the economy worsens, a performing note can quickly become non-performing. Helping late-paying borrowers avoid losing their homes[4] may let them recover financially and start paying on time.

Other factors, besides payment performance, influence whether a mortgage note remains an asset or becomes a liability. Here are three common factors:

- Lien position. Owning a first-position note means you’re first in line to get paid if the home is sold after foreclosure[5]. But if you have a second-position performing note, it may become a liability if the borrower defaults.

- Seasoning. Seasoning refers to how long the borrower has paid the mortgage. A new performing note might be a hidden liability since the borrower hasn’t proven long-term payment reliability.

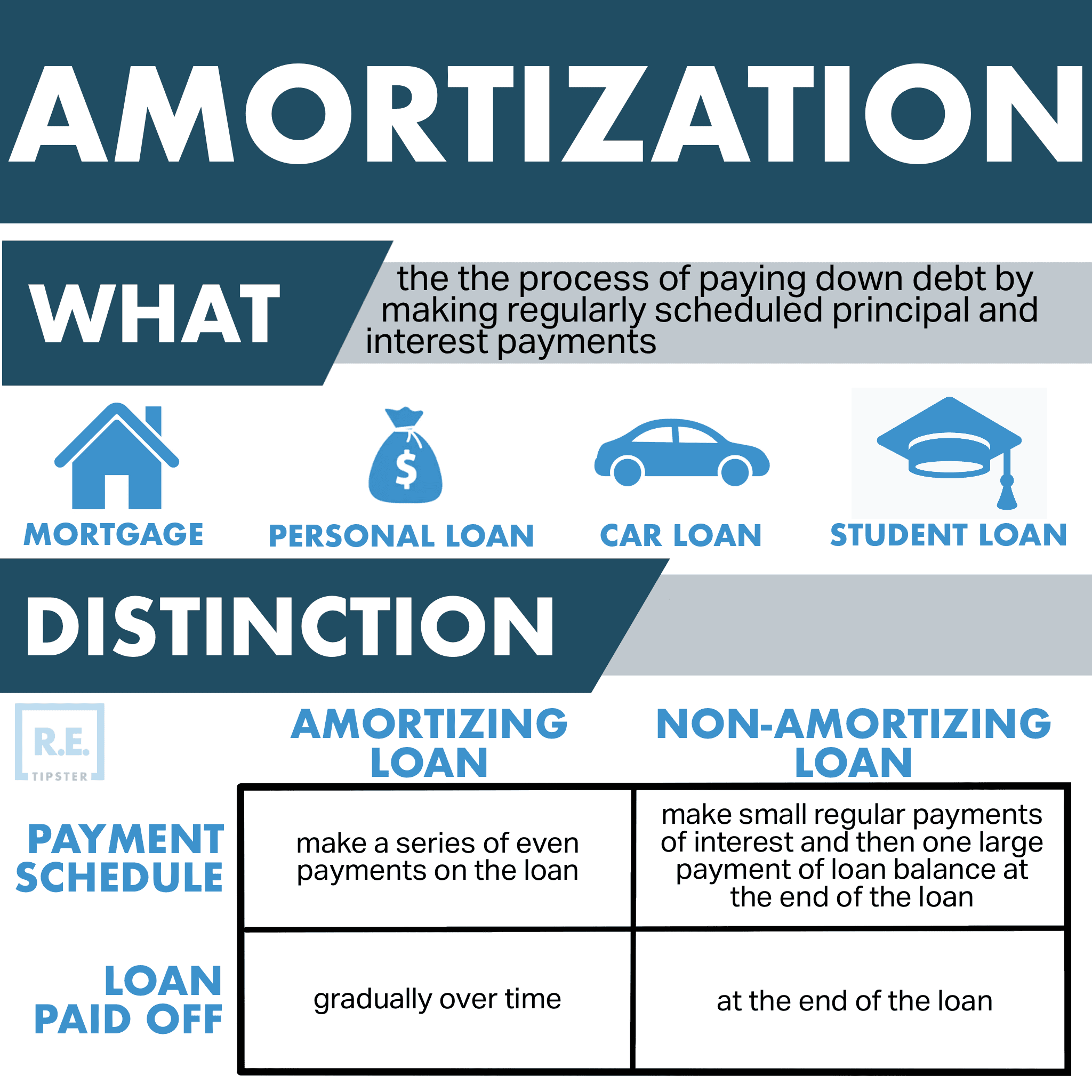

- Amortization. In amortized notes, parts of each payment go to interest and principal[6]. Since interest is based on the remaining principal, your income decreases over time.

On the other hand, with notes tied to interest-only loans, the entire monthly payment goes to interest. The principal stays the same and is due when the note matures.

Comparison of Notes to Similar Terms

Notes are similar to other financial terms.

Note vs. Loan

A note is a legal document showing that a borrower owes money and repayment terms. A loan is the actual sum of money lent for a specific purpose.

In real estate, notes can be for residential, commercial, or industrial properties.

RELATED: State-Specific Loan Documents: What’s Right for You?

Loans can be installment-based or lines of credit. Installment loans provide all the money upfront with fixed payments. They end once you pay them off since they are non-revolving.

On the other hand, lines of credit give access to a specific amount of cash. Interest only builds on the amount you use, and they’re a type of revolving credit, so you can reuse what you pay back.

Loans can be without collateral (unsecured) or with collateral (secured). Payday loans are unsecured[7], while car title loans are secured[8]. By contrast, real estate notes are always tied to mortgages, making them always secured.

Note vs. Mortgage

Since it’s a document, a note describes the loan’s terms and conditions, while a mortgage refers to the property used as collateral.

Mortgages are often thought of as home loans but can also be used for other properties like townhouses, condos, mobile homes, or land for farming or business.

Note vs. Debt

A note represents a debt that the borrower must repay.

As a performing note investor, you become a creditor. This can be favorable, as you’ll work with borrowers who pay on time and likely take their financial responsibilities to you seriously.

Note vs. Deed

A note is a signed agreement between the seller and buyer, outlining the loan amount, interest rate, repayment time, and other key details.

The deed is the document that transfers property ownership from one person to another. Different types of deeds[9] offer varying levels of protection against future claims.

Sources

- Landlord Responsibilities and Duties of a Tenant. (2020, February 27.) Zillow. Retrieved from https://www.zillow.com/rental-manager/resources/landlord-rental-maintenance-laws/

- Hedge funds investing in delinquent mortgages. (2008, July 31.) NBC News. Retrieved from https://www.nbcnews.com/id/wbna25939227

- The Mortgage Servicing Collaborative. (2022, December 15.) Urban Institute. Retrieved from https://www.urban.org/policy-centers/housing-finance-policy-center/projects/mortgage-servicing-collaborative/help-me-understand-mortgage-servicing/what-mortgage-servicing

- Lee, J. (2022, August 4.) How to stop foreclosure. Bankrate. Retrieved from https://www.bankrate.com/mortgages/how-to-avoid-foreclosure/

- Loftsgordon, A. (2023, February 28.) What Happens to Liens and Second Mortgages in Foreclosure? Nolo. Retrieved from https://www.nolo.com/legal-encyclopedia/what-happens-liens-second-mortgages-foreclosure.html

- Robertson, C. (2021, August 21.) PITI: Find Out All That Goes Into Your Mortgage Payment. The Truth About Mortgage. Retrieved from https://www.thetruthaboutmortgage.com/what-does-a-mortgage-payment-consist-of/

- Do I have to put up something as collateral for a payday loan? (2022, January 17.) Consumer Financial Protection Bureau. Retrieved from https://www.consumerfinance.gov/ask-cfpb/do-i-have-to-put-up-something-as-collateral-for-a-payday-loan-en-1595/

- Gellerman, E. (2021, October 31.) How do title loans work? Credit Karma. Retrieved from https://www.creditkarma.com/personal-loans/i/how-do-title-loans-work

- 6 Types of Deeds in Real Estate Explained. (2021, September 8.) MasterClass. Retrieved from https://www.masterclass.com/articles/types-of-deeds