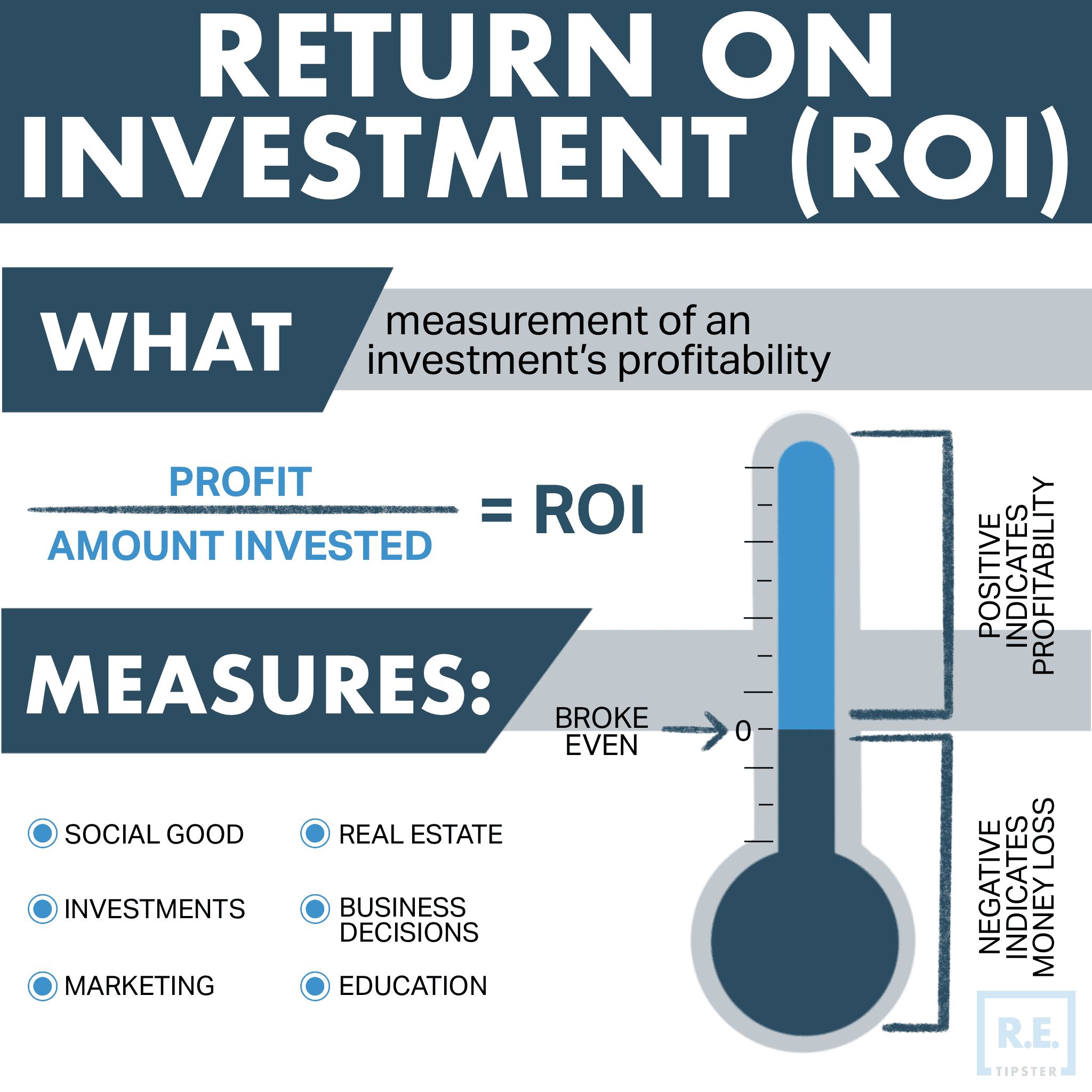

What Is Return on Investment (ROI)?

REtipster does not provide tax, investment, or financial advice. Always seek the help of a licensed financial professional before taking action.

Return on Investment (ROI) Explained

Return on investment, or ROI, is one of the simplest calculations in the financial world.

ROI is a ratio: your net gain (or loss) on an investment, over the total amount you invested. It’s expressed as a percentage.

If you invest $10 and get your initial $10 back plus $1 in profit, how much a return did you earn?

You would have earned a 10% return: your $1 profit equals 10% of your $10 investment.

An ROI calculator not only helps you run the numbers on past investments, but it can also help you forecast returns on future investments. It allows you to compare multiple investments to determine the most promising – and can help you avoid making bad investments entirely.

A $1 profit, divided over a $10 investment, equals an ROI of 10% ($1 / $10 = .1 or 10%).

It can also be used to express losses. If you invested $10 but only got $8.50 back, you lost $1.50 so your ROI would be -15%.

The beauty of ROI lies in its simplicity. You use the ROI formula to calculate one-time gains (such as the profit from flipping a property), or ongoing annual income (such as net cash flow from a rental property). When you calculate ROI for ongoing income, it’s often referred to as annual yield, as it measures the total annual income generated by your initial investment.

Return on investment tells you how efficient an investment is and how effectively it is generating profit for you. It answers the simple question of how much money you can expect in profit for each dollar you invest.

ROI Calculator

The ROI Formula

You can calculate ROI on the back of a cocktail napkin, and there are a couple of different ways to do it (both will give you the same result).

One formula looks like this:

Using this formula, if you bought a parcel of land today at a cost of $5,000 and sold it tomorrow for $10,000, your ROI would look like this:

Another abbreviated way to calculate the formula is like this:

Note that the “Net Profit” number is essentially the same thing as “Gain from Investment – Cost of Investment”.

Bear in mind that the ROI formula only measures upside, or profit, without measuring the downside of risk. It tells you how much money you stand to earn (or have already earned) on an investment, but nothing about the odds of losing money.

ROI Calculation Examples

As touched on above, different investments return money in different ways. You can use the ROI formula for any investment type, even for investments that seem like apples and oranges.

Consider three examples, where you invest an imaginary $100,000.

Example 1: Flipped House

You invest $65,000 in a fixer-upper house, plus $4,000 in closing costs, $30,000 in home renovation costs, and another $1,000 in carrying costs. Total investment: $100,000.

A few months later you sell the renovated property for $130,000. After the expenses of your second round of closing costs, you net $25,000.

You divide that $25,000 profit over your cash investment of $100,000 to calculate your total return at 25%. A fantastic return, especially in such a short time frame, by most standards.

But keep in mind that the return on investment calculation does not include your labor in this case. You may have delegated all the work to a partner or general contractor and never broken a sweat. Or you may have put in 200 hours of hard labor, and the ROI calculation wouldn’t be able to tell you the difference between the two scenarios unless you subtracted your labor costs from your profits before entering them.

Example 2: Rental Property

Imagine you finish the renovations on that house above and decide to keep it as a rental property instead.

The property rents for $1,500 per month, but not all of that is profit. You’ve made that real estate investing mistake before, and know you have to subtract for expenses including:

- Vacancy rate

- Property taxes

- Property insurance

- Repairs and maintenance

- Property management fees

- Bookkeeping, accounting, legal, travel, and miscellaneous expenses

All in all, those expenses often add up to around 50% of the rent. After running the numbers, you discover that this property comes with non-mortgage expenses that average $750 per month over the long term.

To calculate the return on investment – as annual income, in this case – you multiply the average monthly profit of $750 by 12 to reach $9,000 in annual profit. Then, you divide that yearly profit by your total cash investment of $100,000, for an annual return of 9%.

Example 3: Stocks

In this case, you buy shares in a stock index fund. When you buy, the share price is $50, so $100,000 gives you 2,000 shares. You wait a year to sell (to avoid short-term capital gains tax), and then you sell your 2,000 shares for $54 apiece. In other words, you invested $100,000, and you got back $108,000.

So, you earned an $8,000 profit on a $100,000 investment. The calculation looks like this: $8,000 / $100,000 = .08 or an 8% return on investment.

Now let’s add a twist. Say the index fund paid a 2% dividend yield, meaning that it pays 2% annually in dividend income. Over the course of that year that you owned shares, you received $2,000 in dividends on your $100,000 investment.

That means that by the time you sold, you had earned $2,000 in dividends plus $8,000 in capital gains, or $10,000 in total returns. In that case, you earned a 10% return: $10,000 in profits / $100,000 investment.

“Real” Returns: What About Inflation?

ROI calculators don’t typically account for inflation, which sometimes affects your “real” return, depending on the type of investment.

Some investments adjust automatically for inflation. For example, landlords can raise the rent every year, keeping pace with or even exceeding inflation. Other investments, such as flipping houses or flipping land, complete so quickly that inflation is virtually irrelevant.

RELATED: INSANE ROI from One Land Deal!

But some investments lose money to inflation. Imagine you invest $100,000 in one-year bonds that pay 3%. However, if inflation runs at 2% that year, then your “real” return is only 1%. At the end of the year, you get $103,000 back, but it takes $102,000 today to buy what $100,000 bought last year.

Cash-on-Cash Returns

In the real estate investing world, one specific type of return that investors often calculate is cash-on-cash return. Investors calculate it when they use financing to buy a property, to focus on the return on their own personal cash invested.

Take the house flipping example above, where the investor planned to invest $100,000 total and earn $25,000 in profits. Imagine instead that they took out a purchase-rehab loan, where the lender covered 80% of the purchase price and 100% of the renovation costs.

The math for the investor’s own money suddenly changes. Now, they only invest $13,000 of their own cash toward a down payment and nothing toward renovations. That said, both their closing costs and their carrying costs go up due to lender fees and interest. Instead of $4,000 in closing costs and $1,000 in carrying costs, let’s say they now pay $6,500 and $3,500 respectively ($10,000 total instead of $5,000 total).

So, the investor comes up with $23,000 of their own money. That extra $5,000 in loan-related costs drops their total profit from $25,000 to $20,000.

Their cash-on-cash return, therefore, is calculated as their $20,000 profit over their $23,000 cash investment, for a total cash-on-cash return of 87%. A rather large difference in the return they earn on their money, eh?

Pros and Cons of ROI Calculations

Calculating return on investment has its pros and cons. As you evaluate potential investments, keep in mind these advantages and limitations.

Advantage #1: Simplicity

You only need two numbers to calculate ROI: the profit (or loss), and the amount initially invested. Using an ROI calculator like this one makes it even easier.

Advantage #2: Easy Investment Comparison

Should you invest your money in Investment A or Investment B? All else being equal, if Investment A will yield a 10% return while Investment B only an 8% return, then you confidently move forward with Investment A knowing that your money will work harder for you.

Limitation #1: Ignores the Factor of Time

In the real world, time plays an important role in your returns. If two investments both yield 10%, but you get your money back within one year in Investment A and have to wait three years in Investment B, then clearly Investment A is the better investment. But you wouldn’t know that simply by looking at the ROI numbers.

Limitation #2: Ignores Risk

Likewise, imagine two investments both yielding 10% ROI. But one of them is extremely safe, while the other is extremely high-risk. Obviously, you should choose the safe investment that offers the same return, but ROI by itself contains no information about risk.

Limitation #3: Profit & Investment Figures Subject to Optimism, Omission, and False Assumptions

Like any calculation, the result is only as valid as the numbers you input. But in the case of ROI, it’s all too easy to ignore crucial variables when calculating both your potential profits and your investment amount.

For example, when they calculate ROI for a real estate investment, novice investments often overestimate their returns by ignoring closing costs. Or they may underestimate their ongoing expenses, such as vacancy rate or the cost of repairs and maintenance.

Final Thoughts

For every investment you ever make, you should calculate your anticipated ROI.

In some cases, those numbers will be precise, such as when you calculate returns on a rental property or house flip, or when you buy a newly issued bond. In other cases, such as index funds, all you can really look at are historic returns as an indication of what you should expect.

But ROI is just one of several lenses to view any prospective investment through. You should also consider the time horizon of the investment, the risk, the impact of inflation, the liquidity, and the opportunity cost of investing in one asset over another. Most of all, you should diversify your investments so that you don’t put all your eggs in one basket.

Return on investment makes a great starting point as you evaluate an investment, but it is only one of several factors you should consider before shelling out thousands of hard-earned dollars.