REtipster features products and services we find useful. If you buy something through the links below, we may receive a referral fee, which helps support our work. Learn more.

If you're trying to sell a property with owner financing and want to understand how the process works, I will show you the process I go through when closing this type of real estate transaction with a Land Contract (Contract for Deed).

Disclaimer: A land contract is not the right loan instrument for every seller-financed transaction (more about that in this blog post). The goal of this blog post is not to replace a professional closing agent or suggest what type of loan documents you should be using. The goal is to educate you about how land contract closings work so you understand the significance of each document and step in the process.

I am not an attorney or CPA; this information is not legal advice. This is also not a suggestion that you should (or shouldn't) use a land contract or close your own deals. Every state has different laws, and every transaction has unique variables that can affect the documents and steps listed below. Before you act on anything described here, please work with a licensed, qualified attorney in your area to ensure you're using the right documentation and following the right procedures.

⚠️ SELLER FINANCING WARNING: Seller financing creates ongoing legal relationships and significant liability exposure. Always verify the buyer's creditworthiness, identity, and legal capacity. Land contracts involve complex foreclosure procedures that vary by state.

DO NOT SELF-CLOSE SELLER-FINANCED DEALS IF:

- You lack experience with foreclosure laws.

- The buyer cannot provide full financial documentation.

- Property value exceeds $20,000.

- You're uncomfortable with ongoing liability.

- Your state has complex foreclosure requirements.

Ready to see the exact steps I go through when I sell vacant land with a land contract? Let's dive in!

The Closing Checklist

When closing a land contract in-house, these are the basic steps I go through.

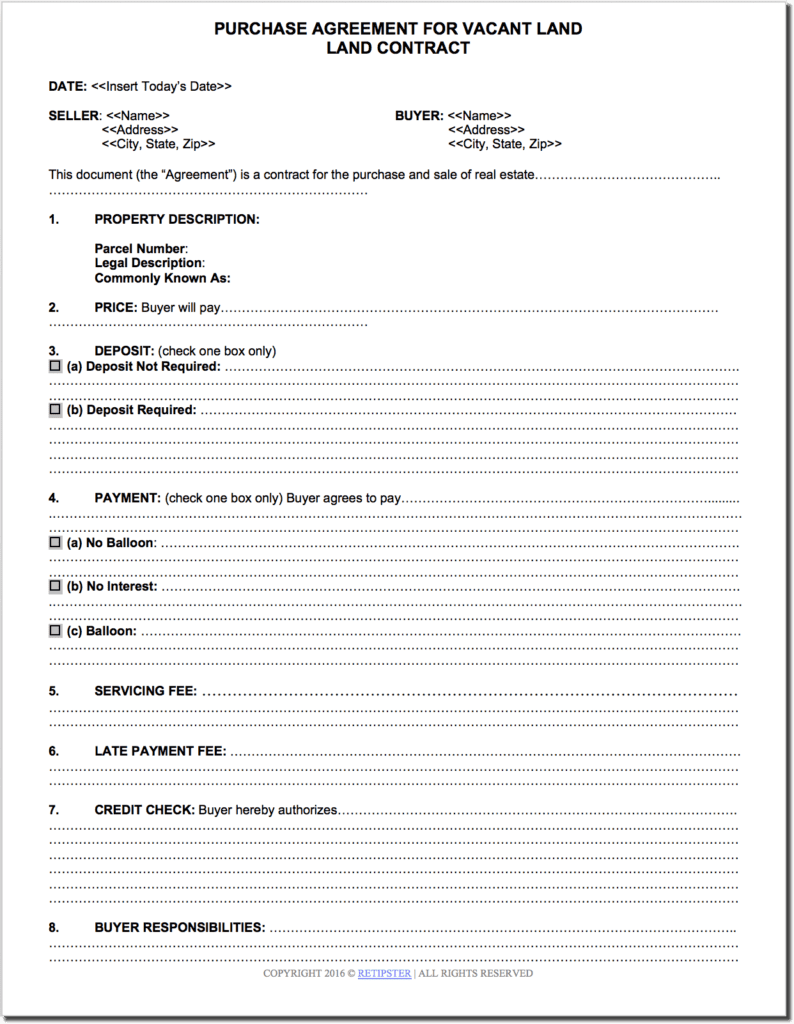

1. Purchase Agreement

As with any real estate deal, it all starts with signing a Purchase Agreement between both parties.

This document spells out the Buyer's and Seller's intentions, putting all the pertinent details in writing.

With any seller-financed real estate deal, the purchase agreement is very important because it establishes all the financing arrangement, such as:

- Sale Price

- Interest Rate

- Term (Duration) of the Loan

- Closing Costs

- Servicing Fees

- Late Payment Fees

- Prepayment Penalties (if any)

- Escrow Arrangements (if any)

- Earnest Deposit (if any)

- Inspection Period

- Closing Deadline

- Etc.

Unlike a cash transaction (where the buyer and seller go their separate ways after closing), a seller-financed transaction creates an ongoing relationship between both parties.

When the deal is closed, the buyer and seller become a borrower and lender, and they will continue to deal with each other for the remainder of the loan term. Both parties must agree on their respective commitments to the deal and to each other.

When I sell properties with a land contract, I work with raw land, and only use land contracts in states where the state law makes the foreclosure process easy.

Since vacant land is a relatively simple property type (with no tenants to deal with, no improvements to inspect, no utility bills to worry about, etc.), my purchase agreement doesn't need to be long and confusing. The terms I offer my buyers are very similar from one deal to the next, and because of this, I can use a very simple template to get the job done.

My contract is three pages long, and it looks something like this:

Filling out all of these details at the outset takes a few minutes, but once it's finished and both parties have signed it, all the subsequent steps become MUCH easier because this agreement spells out all the details you'll need to insert into the Land Contract (Step 3, below).

Need to generate a loan payment schedule? With this calculator, you can solve for the term, interest rate, principal, or payment. Enter three (3) of the four known fields, then press the button next to the empty field to calculate!

Once calculated, click “View Amortization Schedule” to see the results!

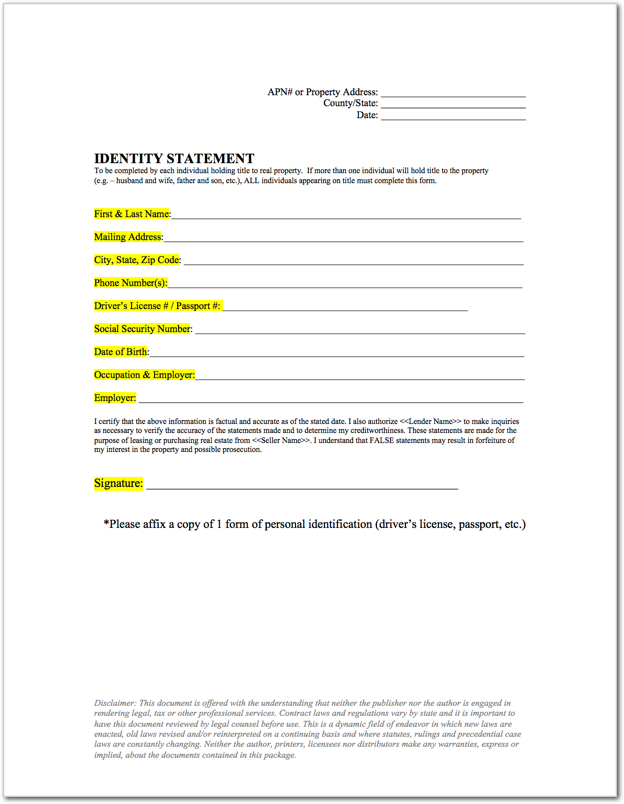

2. ID Statement

A personal identity statement is another simple form that is very helpful as you prepare the documents to close a seller-financed real estate deal.

Below, you'll see a 1-page document that asks for the following information from the buyer/borrower:

- First & Last Name

- Mailing Address

- Phone Number(s)

- Driver's License or Passport Number

- Social Security Number

- Date of Birth

- Occupation & Employer

- Signature

- Copy of Driver's License or Passport

Here's what mine looks like:

This form accomplishes a couple of things:

- Verifies the FULL legal name of the borrower (which is important to ensure the buyer's information is correct on all the loan documents).

- If the proper language is included, this form can also authorize the seller/lender to pull a personal credit report on the buyer/borrower if needed.

Many title companies and closing attorneys will ask for all the same information when handling the closing. This document will also tell you a very brief but helpful story about your borrower, which is good information to know if you want to understand who you’re working with.

![]() One easy way to handle this form is with an e-signature platform like PandaDoc, where the borrower can answer these questions AND e-sign it simultaneously.

One easy way to handle this form is with an e-signature platform like PandaDoc, where the borrower can answer these questions AND e-sign it simultaneously.

3. Land Contract (aka – Contract for Deed)

While there are several different “instruments” that can be used to close a seller-financed transaction, the Land Contract (sometimes known as a “contract for deed,” “articles of agreement for deed,” “land installment contract,” “bond for title” or “installment sale agreement”) is what I've used most often in my home state of Michigan.

A land contract isn't necessarily the right document to use in every state around the country because some states have laws and statutes that make it difficult to work with in the event of foreclosure. In the states where it is most commonly used, there are variations on the specifics of what this document says, but it generally accomplishes the same purpose.

With a Land Contract, the seller holds the legal title to the property for the entire term of the loan (i.e., the deed won’t transfer to the new buyer until after the loan is paid in full). In the meantime, the buyer will get an equitable interest in the property immediately after the closing.

Some people see a land contract as more favorable for the seller because of how the title is held during the loan term. Still, fundamentally speaking, the result isn't a big variation from what usually happens in a typical lending/borrowing relationship.

Whatever type of loan instrument you decide to use (land contract or otherwise), take the time to read this document carefully. Every state has differences in how this form is written, so you'll want to understand what you and your buyer agree to. As you read it through, you’ll see that most of the information isn't surprising, but it will help you understand the responsibilities of both parties for the life of the loan.

4. Land Contract Memorandum

Depending on how the Land Contract is worded, most sellers will also prepare a Land Contract Memorandum (aka – Memorandum of Land Contract).

The purpose of a Land Contract Memorandum is to act as a recorded notification to the public that:

- The seller currently owns this property.

- This property has been sold to the buyer but is currently on land contract.

This document is signed and notarized by both parties, then recorded at the county Register of Deeds (aka – Recorder's) office.

The Land Contract Memorandum is a simple document, and the purpose is to protect both the buyer and seller. If any third parties conduct a title search on the property before the land contract is paid off, they will find this document, which will help them understand what is happening.

For example:

- If the buyer ever tries to sell the property behind the seller’s back (before the loan is paid off), their new buyer would most likely do a title search, and this memorandum would inform them that the seller still owns the property and the buyer doesn’t have the legal right to sell it yet.

- If the seller ever tries to sell the property to another person behind the buyer’s back (before the loan is paid off), this new buyer would most likely do a title search. This memorandum would inform them that the property has already been sold to someone else, and the seller doesn’t have the right to sell it again unless they go through the proper foreclosure process.

- If any other lender tries to take this property as collateral by placing a lien on the property (for any reason whatsoever), they would do a title search and realize that the seller already has a superior lien on the property, and they will most likely need to be paid off before the loan can proceed.

By recording this document at the county office, it will notify all interested parties that:

- The property is currently owned by Person A

- The property is being sold to Person B

- Person A is financing the sale for Person B via Land Contract

Effectively, this public information should prohibit either party from doing anything dishonest behind the other party’s back.

Of course, all of these scenarios are rather improbable – but it’s still a good practice to get this document signed, notarized, and recorded because it keeps everyone honest (and if you don’t do it, nobody will have any idea what is happening with the property, other than the buyer and seller).

One potential option for a Land Contract Memorandum is to use the Memorandum of Agreement from Rocket Lawyer (note: this particular template is very general and would need a few edits to reference the original land contract).

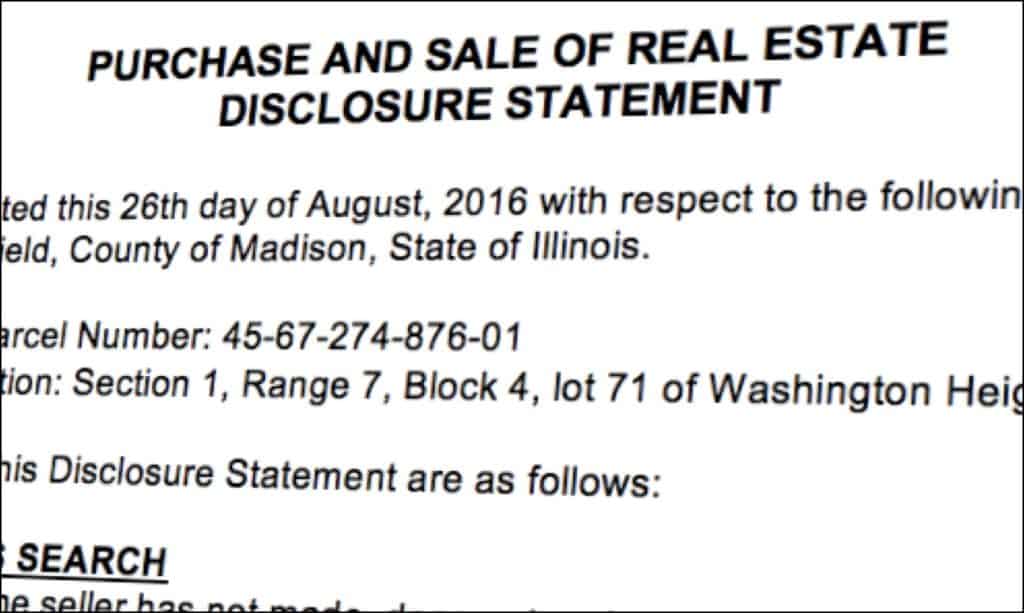

5. Disclosure Statement

The purpose of this form is to ensure that when a property is sold, the buyer is responsible for doing their due diligence, not the seller.

The purpose of this form is to ensure that when a property is sold, the buyer is responsible for doing their due diligence, not the seller.

When buying and selling properties quickly, I don't always have time to research every potential issue under the sun. I make a point of investigating the most common issues that are relevant to me, but since it's almost impossible to know everything, this document confirms a few things in writing:

- The buyer understands it's their responsibility to do their homework before they purchase the property. The seller won't be blamed for the buyer's failure to investigate.

- The seller will not assume any liability or responsibility for issues they were never aware of in the first place.

- The buyer is releasing the seller of all liability in the transaction (i.e., they won't come after the seller at the first sign of trouble).

Don't get me wrong, I've never even come close to getting sued or encountering legal issues with this type of thing, but if I ever did, a statement like this would be very helpful to have in my corner. This is why I've made it a required document that gets signed every time I sell a property.

It's also worth noting that some states have specific disclosures required in every closing scenario, so you'll want to investigate whether there are any additional forms you should complete as required by your state.

6. Closing Statement

A Closing Statement spells out the “math equation” behind the transaction. It shows how much of a down payment the borrower is bringing to the table, what the closing costs will be, what portion of the sale price is being financed, and more.

A closing statement is really just basic math. However, for someone who isn't accustomed to them, compiling a closing statement can require a bit of thought, especially if it involves complicated fees or prorations.

This document can be confusing, so it's important that they are completed correctly.

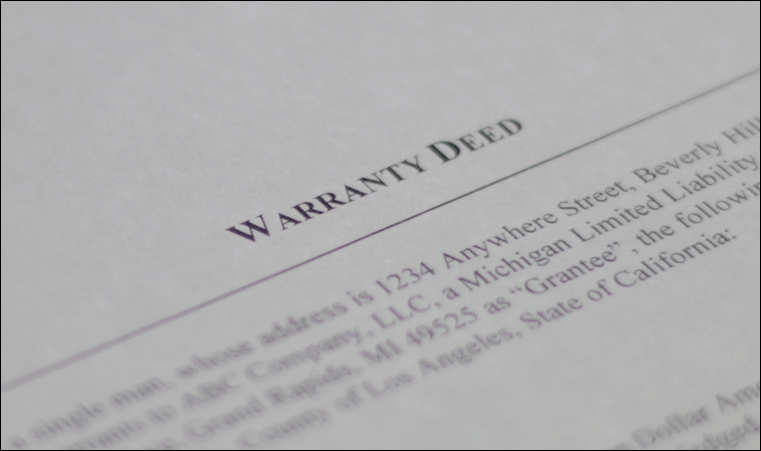

7. Deed

One unique attribute of a land contract is that the seller doesn't deliver the deed to the buyer until the loan is paid in full.

One unique attribute of a land contract is that the seller doesn't deliver the deed to the buyer until the loan is paid in full.

Even so, most loan servicing professionals recommend creating this document at the time of closing and putting it in a safe place (or giving it to an escrow company) until the loan is paid in full.

Why create the deed at the time of closing?

Because if anything ever happens to the seller/lender before the loan is paid off (i.e., if the seller dies in a tragic accident or becomes physically unable to sign legal documents for any reason), the deed will already exist, and when the buyer/borrower fulfills their end of the deal, it can easily be delivered to them rather than going through a long, drawn-out and unnecessary court procedure for something that should have been cut-and-dry if the deed had been prepared and executed at the time of closing.

Either way, the deed shouldn't be recorded or given to the buyer until AFTER the loan has been paid in full.

Several different types of deeds can be used when transferring real estate (and the types can vary by state). Let's cover a few of the most commonly known ones and what implications are inherent in each one…

Warranty Deed

With a Warranty Deed, the seller is giving the buyer their “Warranty” (i.e., Guarantee/Promise) that the title to the property is free and clear, and the buyer will receive all reasonable rights to the property. This type of deed should only be used when the seller knows the property's title is clear of any liens and encumbrances.

Most educated buyers will strongly prefer this type of deed (and if a lender gets involved – it will almost always be required).

Most sellers are okay with signing a Warranty Deed because:

- This was the same thing they received when they bought the property.

- They paid for a title insurance policy when they purchased the property, which ensures a clear title and protects them from any issues (should they arise).

Don't use a Warranty Deed if you’re not certain you have a clear title to the property you're selling.

Quit Claim Deed

With a Quit Claim Deed, the seller offers no warranty concerning the property’s title. In essence, the seller isn’t even claiming to have any ownership in the first place. By signing this document, the seller is saying,

“Whatever interest I may have in this property (if anything), I am transferring it to the buyer.”

If a buyer is willing to accept this, they should do their homework to ensure the property has a clear chain of title.

Because of how open-ended this type of deed is, it tends to create problems in the chain of title for future owners since it lacks any guarantees or clear statements about who owns the property. If the seller’s goal is to simply not guarantee the title from the beginning of time, another alternative is to issue a Special Warranty Deed (more on that below).

Special Warranty Deed

An alternative to the Warranty Deed and the Quit Claim Deed is the Special Warranty Deed. In most cases, this type of deed is used when the seller is willing to guarantee that no defects occurred with the property's title when they owned it.

With a Special Warranty Deed, the seller ISN'T necessarily saying the property has a spotless record going back to the beginning of time; only that it accrued no defects during their period of ownership (there's a big difference – and a Special Warranty Deed can help you spell this out).

8. Supporting Documentation

Many states require some additional “supporting documentation” to notify the local municipality (i.e., City or Township) about the transaction that occurred.

The county should be fully aware of this change in ownership because they recorded your deed. Still, in many cases – the city or township administration is in a separate office, and they don't share the same systems with the county. As such, they need to be notified separately about the property's change in ownership (and if they aren't made aware of the change, they'll continue sending the property tax bills to the old owner).

In most cases, this is a simple, one-page form that serves a few key purposes:

- Lets the city/township know that the property has been transferred to a new owner.

- Informs the local Assessor of the sale price (which assists them in determining the new assessed value of the property).

- Notifying the local treasurer who/where they should send all future tax bills.

Unfortunately, the exact name of this document varies quite a bit from state to state, so even though it serves the same basic purpose, it can seem a bit more complicated than it is. For example:

-

- In Arizona, it's called an “Affidavit of Property Value” and it looks like this.

- In Michigan, it's called a “Property Transfer Affidavit” and it looks like this.

- In Nevada, it's called a “Declaration of Value” and it looks like this.

- In Maine, it's called a “Real Estate Transfer Tax Declaration” and it looks like this.

- In Hawaii, it's called a “Conveyance Tax Certificate” and it looks like this.

If you're unsure whether your state requires this form, this video explains how you can figure it out…

See what I mean? Hopefully, you get the idea.

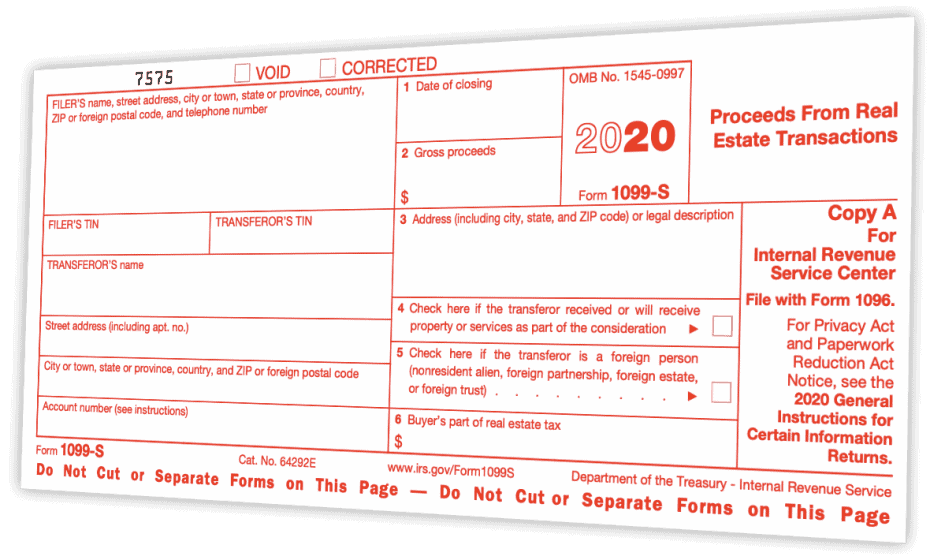

9. IRS Form 1099-S

In many (though not all) situations, the person responsible for closing the transaction must file Form 1099-S with the IRS.

In many (though not all) situations, the person responsible for closing the transaction must file Form 1099-S with the IRS.

There are some instances where this form isn’t required, but as a general practice, if you’re planning to facilitate the signing of these closing documents yourself, it’s a good idea to either:

- Plan on filing this form yourself.

- In a written agreement, designate the other party as the responsible person.

Whether you file the form yourself or designate the other party to do so – it’s a fairly straightforward process (but it can take a bit of learning if you’ve never done it before). Learn more about why the 1099-S is important and how you can handle the filing process in your closings.

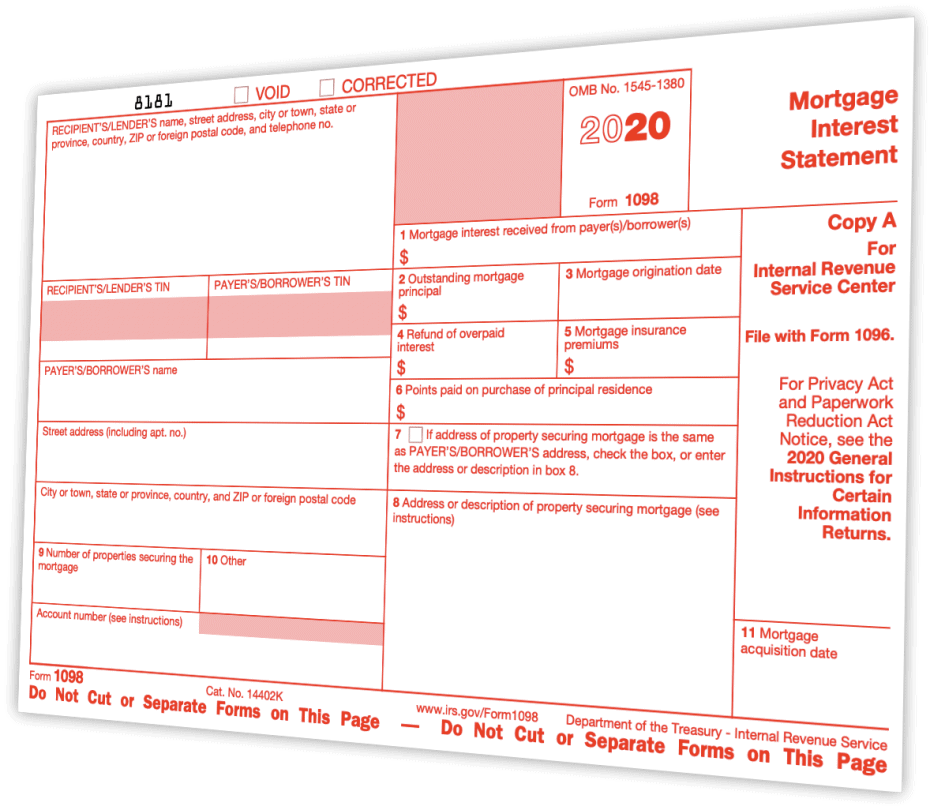

10. IRS Form 1098

If you're doing a substantial number of seller-financed deals AND servicing them yourself, you should also plan on filing Form 1098 with the IRS for every borrower who pays you $600 or more of interest in each fiscal year.

If you're doing a substantial number of seller-financed deals AND servicing them yourself, you should also plan on filing Form 1098 with the IRS for every borrower who pays you $600 or more of interest in each fiscal year.

The good news is – if you're using a loan servicing company or working with a CPA to prepare your annual tax return, one of them will most likely handle this for you (but be sure to check with them to verify).

If you plan to handle this requirement yourself, it's a fairly straightforward process (similar to the 1099-S), but it can take a bit of education to understand the mechanics of it. Check out this blog post for more details.

Record Keeping

Once your Land Contract is closed, the documentation is complete, and the appropriate documents have been recorded by the county, be sure to keep copies of ALL fully executed documents (and if you haven't already, make copies of all the documents and send them to the other party for their records as well).

All the copies I keep in my system are digital (in pdf format), and I keep a pretty clean filing system with individual folders for each borrower. I’d recommend figuring out a similar system and backing up your files.

Post-Payoff: Record or Deliver the Deed

When the buyer has made their final payment (years from now), it is the seller’s duty to provide the original signed and notarized deed to the buyer and/or get the document recorded, transferring the legal title of the property to the buyer. This will confirm that the borrower has paid the loan in full and will eliminate any associated liens (e.g., the Land Contract Memorandum) from the property's chain of title.

If the deed was created at the time of closing (and it should be), it could be held in escrow by a title company or designated attorney for the loan payoff period. The title/escrow agent should be notified of the payoff when it happens, so they can take the final steps to finish this process.

Note: As part of the closing process, it's not a bad idea to make sure the borrower has the contact information for whichever party is holding the deed, so the borrower can follow up and close the loop in case the lender is not around to tie up these loose ends when the time comes.

Vacant Land Liability Insurance

Remember, since the seller (that's you) holds title to the property until the land contract is paid off, they also hold all the liability and risk exposure during that time.

As such, you'll want to consider getting liability insurance to cover yourself until that deed is transferred after the final payment.

![]() NREIG has a specific vacant land liability insurance product that works well for this purpose. I'll explain how it works in this short video.

NREIG has a specific vacant land liability insurance product that works well for this purpose. I'll explain how it works in this short video.

You can find the signup form on this page to get started with them.

Document Templates

![]() By now, you've seen the documentation and detail required to close a seller-financed real estate transaction.

By now, you've seen the documentation and detail required to close a seller-financed real estate transaction.

For most people, this job is best left to a professional closing agent (a title company or attorney) who is well-versed in these steps and handles this job every day.

There are plenty of opportunities to make mistakes in this closing process, and even if you do get everything right, it can take a lot of time and mental energy to get this job done!

In my first several years of closing my deals in-house, I used US Legal and Rocket Lawyer for most of the document templates I needed because they have every template you can imagine, and they make the process easy.

In my first several years of closing my deals in-house, I used US Legal and Rocket Lawyer for most of the document templates I needed because they have every template you can imagine, and they make the process easy.

These days, I outsource all of this work to a title company or attorney, because they're better at the job than I am, and it frees up a lot of my time to do more important things in my business.

Whatever you decide to do, it's beneficial to understand what's going on in each closing, so you can make sense of “how the sausage is made.”

When Should You NOT Utilize Seller Financing?

The more you learn about selling properties with owner financing, the more you might start asking yourself,

“Is it really worth the extra effort to sell my properties this way?”

It's a good question because, in my opinion, there are plenty of scenarios where it's not worth the extra time and hassle to offer seller financing to your buyers.

Getting into a seller-financed deal with someone is a real commitment, and it's important to set clear boundaries so you know when to say “No.”

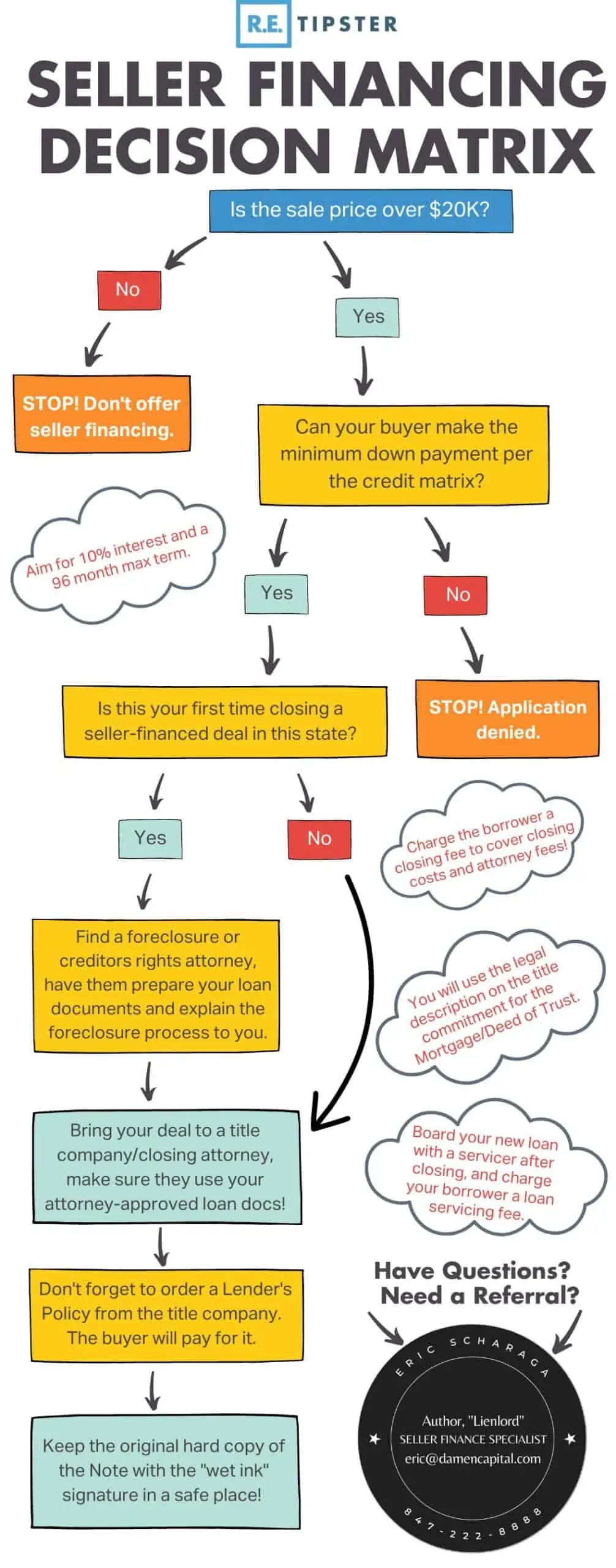

Here's the decision matrix I use to decide on the direction of each deal.

- If the sale price is less than $20K, I don't offer owner financing at all.

- If a property sells for $20K or more, and the buyer wants owner financing, I'll outsource the closing to a title company or attorney.

- If it's my first seller-financed transaction in that state, I'll find a foreclosure/creditors rights attorney to compile the correct loan documentation and help me understand what the foreclosure process looks like.

- If it's not my first seller-financed transaction in that state, my title company will use my attorney-approved templates to close the deal.

- Whatever costs are needed to close the deal, I'll have the borrower pay a minimum $500 closing fee (maybe higher, in some cases) to help offset the costs.

With these guidelines in place, I can only use seller financing on deals that are worth the trouble, and the borrower pays a good portion of the costs, so it doesn't come off my bottom line.

Here's a flowchart I put together with Eric Scharaga (note investor and seller financing aficionado) to help you visualize this decision-making logic.

Seller financing is a huge convenience we can provide for buyers, but we aren't obligated to do this, especially if it doesn't make good financial sense for us.

As a seller, you can choose when you do and don't want to make this available for each buyer. You don't have to follow the same logic explained above, but if you have no idea how to make this decision, this is a decent place to start.

When Should You NOT Use a Land Contract?

Since we're on this subject, it's important to point out that there are many valid reasons NOT to use a land contract, depending on the situation and the state where you're working.

Eric Scharaga explains several of the problematic issues in this conversation.

RELATED: Reasons NOT to Use a Land Contract (ft. Eric Scharaga)

Need More Help?

When I was closing my first few deals, I had a TON of questions, and it would have been very helpful if someone could have held my hand and thoroughly explained what each document was all about, what kinds of issues to watch out for, and how to navigate through each step of the process.

![]() With this in mind, I spent several months creating a full-blown course explaining how this process works from start to finish. The course is designed specifically for people working in the land investing business. It comes with dozens of video tutorials and document templates that explain each step along the way.

With this in mind, I spent several months creating a full-blown course explaining how this process works from start to finish. The course is designed specifically for people working in the land investing business. It comes with dozens of video tutorials and document templates that explain each step along the way.

The Land Investing Masterclass has a BIG module about seller financing (see Module 8). If that sounds helpful, be sure to check it out!